What percentage of income tax is paid by the top 1%? According to data from income-partners.net, the top 1 percent of taxpayers paid 25.9 percent of the average income tax rate in 2021, nearly eight times higher than the bottom half of taxpayers. By understanding these income tax dynamics, businesses and investors can strategically align for increased revenue, lucrative partnerships, and optimized marketing campaigns.

Are you looking to elevate your financial acumen with insights into tax contributions and high-income earners? Income tax insights, strategic partnerships, and optimized marketing are all interconnected aspects of financial success.

1. Understanding the US Federal Income Tax System

The US federal income tax system operates on a progressive tax structure, meaning that individuals with higher incomes pay a larger percentage of their income in taxes. This system is designed to ensure that those who have the greatest ability to pay contribute a larger share of government revenue.

What is Progressive Taxation?

Progressive taxation is a system where the average tax rate increases as the taxable amount increases. In other words, wealthier individuals pay a higher percentage of their income in taxes compared to lower-income individuals. This is based on the principle of ability to pay, where those with more resources contribute more to public services.

How Does the US Federal Income Tax System Work?

The US federal income tax system is based on tax brackets, each associated with a different tax rate. As your income increases, it moves into higher tax brackets, and you pay the corresponding rate on that portion of your income. For example, in 2021, the tax rates ranged from 10% to 37%, depending on income level and filing status.

The Role of the IRS

The Internal Revenue Service (IRS) is responsible for collecting taxes and administering the federal tax laws. It provides data, tables, and statistics that reveal how different income groups contribute to the overall tax revenue. This data is crucial for understanding the progressivity of the tax system and the impact of tax policies on various income levels. The IRS ensures compliance with tax laws and provides resources and guidance to taxpayers.

2. Key Findings from the IRS Data for 2021

In 2021, the IRS released comprehensive data on individual income taxes, providing insights into the contributions of different income groups. These findings highlight the progressive nature of the federal income tax system and the significant role played by high-income taxpayers.

Total Tax Returns Filed and AGI

In 2021, taxpayers filed 153.6 million tax returns, reporting more than $14.7 trillion in adjusted gross income (AGI). This demonstrates the broad participation in the tax system and the substantial economic activity captured by federal income taxes. The top 1% accounted for 26.3% of the total AGI, showcasing their significant economic influence.

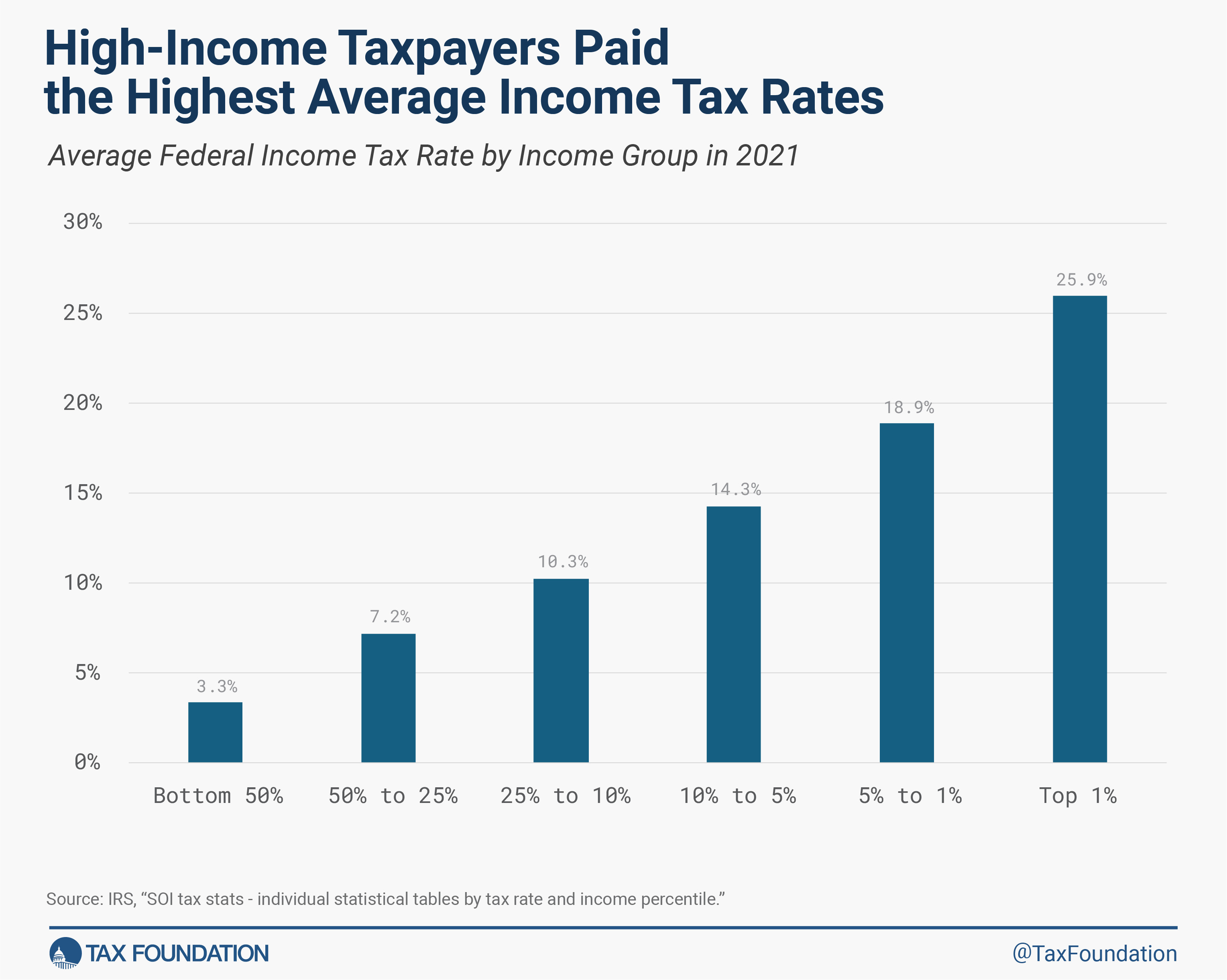

Average Income Tax Rate

The average income tax rate in 2021 was 14.9%. However, the top 1% of taxpayers paid an average rate of 25.9%, nearly eight times higher than the 3.3% average rate paid by the bottom half of taxpayers. This significant difference underscores the progressive nature of the tax system. As incomes rise, so do the average tax rates, reflecting a higher contribution from wealthier individuals.

Share of Federal Income Taxes Paid

The top 1% of taxpayers accounted for 45.8% of all federal income taxes paid in 2021. In contrast, the bottom 50% of taxpayers paid only 2.3% of all federal individual income taxes. The top 50% of all taxpayers paid 97.7% of all federal individual income taxes, while the bottom 50% paid the remaining 2.3%. These figures clearly illustrate that a small percentage of high-income individuals contribute the majority of federal income tax revenue.

Impact of Pandemic-Related Tax Items

The 2021 figures include pandemic-related tax items from the American Rescue Plan Act (ARPA), such as recovery rebates, expanded child tax credit (CTC), and earned income tax credit (EITC). These measures provided tax relief to lower and middle-income groups, affecting the distribution of tax burdens across income levels. The ARPA measures were designed to mitigate the economic impact of the pandemic, particularly for vulnerable populations.

Capital Gains Realizations

Capital gains realizations exceeded $2 trillion in 2021, reaching a 40-year high. This surge in capital gains significantly contributed to income growth and taxes paid for high-income groups. The strong stock market performance in 2021 drove these capital gains, benefiting wealthier individuals who are more likely to hold significant investment assets.

3. Detailed Breakdown of Tax Contributions by Income Group

A closer look at the tax contributions of different income groups reveals the extent to which high-income earners support the federal income tax system. Understanding these contributions can inform policy debates and provide a clearer picture of income distribution and tax burdens.

Top 1%

The top 1% of taxpayers, with an AGI of $682,577 and above, paid an average income tax rate of 25.93%. They earned 26.3% of total AGI and paid 45.8% of all federal income taxes. These figures highlight the significant tax burden borne by the highest income earners. Their contributions are essential for funding government services and programs.

Top 5%

The top 5% of taxpayers earned 42.0% of total AGI and paid 65.6% of all federal income taxes. This group also contributes a substantial share of the tax revenue, reflecting their high incomes and progressive tax rates. The top 5% includes a broad range of high-income professionals and business owners.

Top 10%

The top 10% of taxpayers earned 52.6% of total AGI and paid 75.8% of all federal income taxes. This group includes high-earning professionals, executives, and successful entrepreneurs. Their tax contributions play a critical role in supporting public services and infrastructure.

Bottom 50%

The bottom 50% of taxpayers earned 10.4% of total AGI and paid 2.3% of all federal individual income taxes. While their individual tax burdens are lower, this group benefits from tax credits and deductions designed to provide relief to low-income individuals and families. These credits and deductions help to alleviate poverty and support economic stability.

Table Summary of Federal Income Tax Data, Tax Year 2021

| Category | Top 1% | Top 5% | Top 10% | Top 25% | Top 50% | Bottom 50% | All Taxpayers |

|---|---|---|---|---|---|---|---|

| Number of Returns | 1,535,899 | 7,679,495 | 15,358,991 | 38,397,477 | 76,794,954 | 76,794,954 | 153,589,908 |

| Average Tax Rate | 25.9% | 23.3% | 21.5% | 18.4% | 16.2% | 3.3% | 14.9% |

| Average Income Taxes Paid | $653,730 | $187,468 | $108,251 | $50,963 | $27,891 | $667 | $14,279 |

| Adjusted Gross Income (Millions) | $3,872,395 | $6,182,180 | $7,745,525 | $10,613,602 | $13,191,209 | $1,531,038 | $14,722,247 |

| Share of Total AGI | 26.3% | 42.0% | 52.6% | 72.1% | 89.6% | 10.4% | 100.0% |

| Income Taxes Paid (Millions) | $1,004,063 | $1,439,657 | $1,662,623 | $1,956,857 | $2,141,925 | $51,225 | $2,193,150 |

| Share of Total Taxes Paid | 45.8% | 65.6% | 75.8% | 89.2% | 97.7% | 2.3% | 100.0% |

| Income Split Point | $682,577 | $252,840 | $169,800 | $94,440 | $46,637 | $46,637 | – |

This table provides a concise overview of the tax contributions of different income groups, highlighting the disparities in tax burdens and income distribution. The top 1% and top 5% bear a disproportionately large share of the tax burden, while the bottom 50% contribute a minimal amount.

4. Factors Influencing Tax Contributions

Several factors influence the tax contributions of different income groups, including income levels, tax policies, economic conditions, and demographic trends. Understanding these factors is crucial for interpreting tax data and assessing the impact of policy changes.

Income Levels

Income levels are the primary determinant of tax contributions. Higher-income individuals and households earn more and, therefore, pay more in taxes. Progressive tax rates further amplify this effect, as higher incomes are taxed at higher rates. The distribution of income across different groups also plays a role, as greater income inequality can lead to a larger share of taxes being paid by a smaller percentage of the population.

Tax Policies

Tax policies, such as tax rates, deductions, and credits, significantly influence tax contributions. Changes in these policies can alter the tax burdens of different income groups and affect the overall distribution of tax revenue. For example, the Tax Cuts and Jobs Act (TCJA) of 2017 made significant changes to individual income tax rates and deductions, which had a noticeable impact on tax liabilities across income levels.

Economic Conditions

Economic conditions, such as economic growth, recessions, and stock market performance, can impact tax contributions. During periods of economic expansion, incomes tend to rise, leading to higher tax revenues. Conversely, during recessions, incomes may fall, resulting in lower tax revenues. Stock market performance also plays a role, as capital gains realizations can significantly boost the incomes of high-income individuals.

Demographic Trends

Demographic trends, such as aging populations and changes in household composition, can influence tax contributions. As the population ages, there may be a shift in the distribution of income and tax burdens. Changes in household composition, such as the rise of single-person households, can also affect tax liabilities and the overall tax revenue.

5. Impact of Tax Cuts and Jobs Act (TCJA) on Tax Contributions

The Tax Cuts and Jobs Act (TCJA), enacted in 2017, made significant changes to the federal income tax system. It is essential to assess the impact of these changes on tax contributions across different income groups.

Overview of the TCJA

The TCJA reduced individual income tax rates, widened tax brackets, increased the standard deduction, and made changes to various deductions and credits. These changes were designed to simplify the tax code and provide tax relief to individuals and businesses. However, the impact of these changes varied across different income groups.

Impact on Average Tax Rates

The TCJA generally lowered average tax rates across income groups. However, the magnitude of the reduction varied, with some groups experiencing larger tax cuts than others. The top 1% of taxpayers saw a reduction in their average tax rate, but they still paid a significantly higher rate than lower-income groups. In 2021, average tax rates were lower than in 2017 across all income groups, indicating the lasting impact of the TCJA.

Impact on Share of Taxes Paid

The TCJA also affected the share of taxes paid by different income groups. Some studies have shown that the TCJA led to a greater concentration of tax burdens among high-income earners, with the top 1% paying a larger share of total federal income taxes. This shift in tax burdens has implications for income inequality and the distribution of wealth.

Long-Term Effects

The long-term effects of the TCJA on tax contributions are still being studied. Some analysts predict that the TCJA will continue to benefit high-income earners, while others argue that the tax cuts will stimulate economic growth and benefit all income groups. The actual effects will depend on various factors, including future economic conditions and policy changes.

6. How Pandemic-Related Downturn and Relief Programs Affected the 2021 Data

The COVID-19 pandemic and subsequent relief programs significantly impacted the economic landscape, influencing income levels and tax contributions across different income groups. Analyzing these effects provides insights into the resilience of the tax system and the effectiveness of government interventions.

Economic Downturn

The pandemic led to a sharp economic downturn in 2020, with widespread job losses and business closures. This downturn affected income levels across the board, but the impact was disproportionately felt by lower-income individuals and families. Many low-wage workers lost their jobs or faced reduced work hours, leading to a decline in their income.

Relief Programs

In response to the economic crisis, the federal government implemented several relief programs, including the American Rescue Plan Act (ARPA). These programs provided direct payments to individuals, expanded unemployment benefits, and increased tax credits, such as the Child Tax Credit (CTC) and Earned Income Tax Credit (EITC). These measures aimed to provide financial support to those most affected by the pandemic.

Impact on AGI and Tax Rates

From 2020 to 2021, AGI grew across all income groups on average, but grew faster across higher income groups. The bottom half of taxpayers saw a 20% increase in AGI, while the top half saw a 17% increase. The American Rescue Plan Act (ARPA) provided a third round of recovery rebates of up to $1,400 per eligible individual and dependent, phasing out for single taxpayers with incomes above $75,000 and joint filers with incomes above $150,000. As household income increases, average income tax rates rise.

Changes in Income Distribution

The combination of the economic downturn and relief programs led to changes in income distribution. The share of income earned by the bottom half of taxpayers increased slightly due to the relief programs, while the share earned by the top 1% also increased due to the strong stock market performance. These shifts in income distribution affected the share of taxes paid by different income groups.

7. Capital Gains and Their Role in High-Income Tax Contributions

Capital gains, the profits from the sale of assets like stocks and real estate, play a crucial role in the tax contributions of high-income earners. Understanding the dynamics of capital gains realizations is essential for comprehending the overall tax landscape.

What are Capital Gains?

Capital gains are the profits realized from selling an asset for a higher price than its purchase price. These gains are subject to capital gains taxes, which are typically lower than ordinary income tax rates. Capital gains can be short-term (held for one year or less) or long-term (held for more than one year), with different tax rates applying to each.

Impact on High-Income Earners

High-income earners are more likely to hold significant investment assets, such as stocks, bonds, and real estate. As a result, they are more likely to realize substantial capital gains. These gains can significantly boost their income and tax liabilities. In 2021, capital gains realizations exceeded $2 trillion, reaching a 40-year high. This surge in capital gains significantly contributed to income growth and taxes paid for high-income groups.

Tax Rates on Capital Gains

The tax rates on capital gains are generally lower than ordinary income tax rates. In 2021, the long-term capital gains tax rates were 0%, 15%, and 20%, depending on the taxpayer’s income level. These lower rates incentivize investment and can reduce the overall tax burden for high-income earners. However, the lower rates also mean that capital gains contribute a smaller share of tax revenue compared to ordinary income.

Volatility of Capital Gains

Capital gains realizations are highly volatile and can fluctuate significantly from year to year, depending on stock market performance and other economic factors. This volatility can affect the stability of tax revenue and make it challenging to predict future tax contributions from high-income earners.

8. The Tax Burden on Different Income Percentiles Over Time

Analyzing how the tax burden has shifted across different income percentiles over time provides valuable insights into long-term trends and policy effects. Examining historical data helps reveal how changes in tax laws and economic conditions have impacted the distribution of tax liabilities.

Long-Term Trends

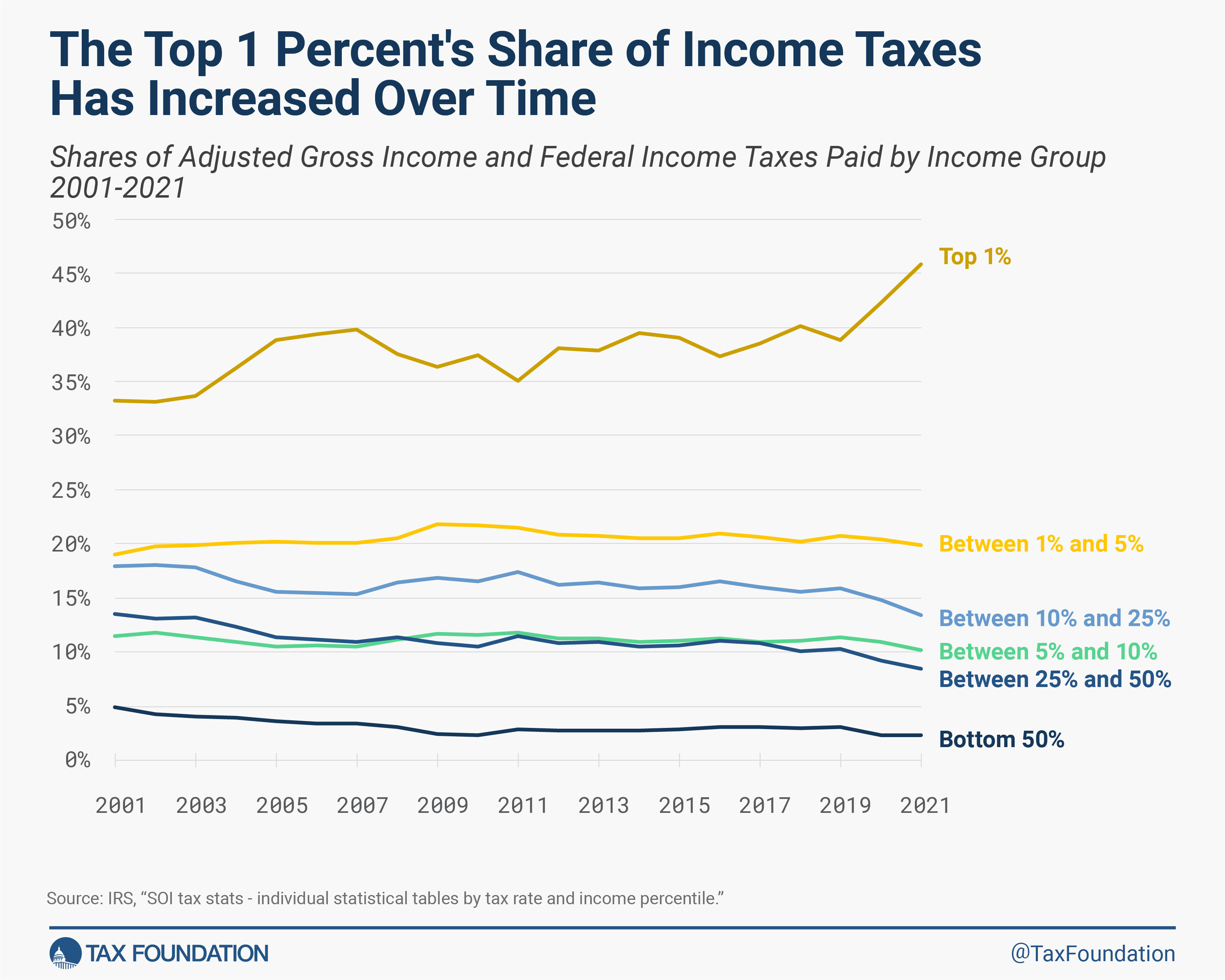

Over the past several decades, there has been a trend toward a greater concentration of tax burdens among high-income earners. The share of federal income taxes paid by the top 1% has increased significantly, while the share paid by the bottom 50% has decreased. This trend reflects a combination of factors, including rising income inequality and changes in tax policies.

Impact of Economic Events

Economic events, such as recessions and stock market booms, have had a significant impact on the tax burdens of different income percentiles. During economic expansions, the incomes of high-income earners tend to rise faster than those of lower-income earners, leading to a greater share of taxes being paid by the top. Conversely, during recessions, the incomes of high-income earners may decline more sharply, reducing their share of taxes paid.

Policy Changes

Changes in tax policies, such as tax rate cuts and increases, have also affected the tax burdens of different income percentiles. Tax cuts tend to benefit high-income earners more than lower-income earners, leading to a shift in tax burdens toward the top. Conversely, tax increases tend to disproportionately affect high-income earners, increasing their share of taxes paid.

Data Tables: Adjusted Gross Income Shares, 1980–2021

| Year | Top 1% | Top 5% | Top 10% | Top 25% | Top 50% | Bottom 50% |

|---|---|---|---|---|---|---|

| 1980 | 12.54% | 32.13% | 24.57% | 56.70% | 82.32% | 17.68% |

| 1990 | 13.62% | 38.77% | 23.36% | 62.13% | 84.97% | 15.03% |

| 2000 | 14.48% | 46.01% | 21.15% | 67.15% | 87.01% | 12.99% |

| 2010 | 18.87% | 45.17% | 22.38% | 67.55% | 88.26% | 11.74% |

| 2020 | 22.19% | 49.45% | 21.26% | 70.71% | 89.82% | 10.18% |

| 2021 | 26.30% | 52.61% | 19.48% | 72.09% | 89.60% | 10.40% |

Data Tables: Total Income Tax Shares, 1980–2021

| Year | Top 1% | Top 5% | Top 10% | Top 25% | Top 50% | Bottom 50% |

|---|---|---|---|---|---|---|

| 1980 | 17.79% | 49.28% | 23.74% | 73.02% | 92.95% | 7.05% |

| 1990 | 18.51% | 55.36% | 21.66% | 77.02% | 94.19% | 5.81% |

| 2000 | 19.05% | 67.33% | 16.68% | 84.01% | 96.09% | 3.91% |

| 2010 | 37.38% | 70.62% | 16.49% | 87.11% | 97.64% | 2.36% |

| 2020 | 42.31% | 73.67% | 14.84% | 88.51% | 97.68% | 2.32% |

| 2021 | 45.78% | 75.81% | 13.42% | 89.23% | 97.66% | 2.34% |

9. Policy Implications of Tax Contribution Data

The data on tax contributions by different income groups have significant policy implications, informing debates about tax reform, income inequality, and government spending. Policymakers can use this data to evaluate the fairness and efficiency of the tax system and make informed decisions about tax policy.

Tax Reform

Tax reform is a perennial topic of debate in the United States. Some argue that the tax system is too complex and inefficient, while others contend that it is unfair and exacerbates income inequality. The data on tax contributions can inform these debates by providing insights into the distribution of tax burdens and the impact of various tax policies. Policymakers can use this data to design tax reforms that promote economic growth, reduce income inequality, and ensure that all income groups pay their fair share of taxes.

Income Inequality

Income inequality is a growing concern in the United States. The data on tax contributions reveal that the share of income earned by the top 1% has increased significantly over the past several decades, while the share earned by the bottom 50% has decreased. This trend has implications for social mobility, economic opportunity, and overall well-being. Policymakers can use tax policies to address income inequality by increasing taxes on high-income earners and providing tax relief to low-income individuals and families.

Government Spending

The data on tax contributions also have implications for government spending. The federal government relies on tax revenue to fund various programs and services, such as national defense, Social Security, Medicare, and education. The data on tax contributions can help policymakers make informed decisions about how to allocate government resources. For example, if the share of taxes paid by high-income earners is increasing, policymakers may consider increasing spending on programs that benefit low-income individuals and families.

Addressing Refundable Tax Credits

When evaluating tax burdens, it’s essential to account for refundable tax credits. Because the Office of Management and Budget (OMB) classifies the refundable part of tax credits as spending, the IRS does not include it in tax share figures. The result overstates the tax burden of the bottom half of taxpayers. Including the refundable portion of tax credits would provide a more accurate picture of the tax burden on different income groups.

Federal income taxes paid across various income levels

Federal income taxes paid across various income levels

Alt: The graph showcases the average effective federal income tax rates across different income levels, highlighting the progressive nature of the tax system.

10. Strategies for Businesses and Investors to Leverage Tax Data

Businesses and investors can leverage tax data to make informed decisions about partnerships, marketing, and financial planning. Understanding the tax landscape can provide a competitive edge and help optimize financial outcomes.

Identifying Strategic Partnerships

Tax data can help businesses identify potential strategic partners by providing insights into the financial health and tax liabilities of different companies. By analyzing tax data, businesses can assess the financial stability of potential partners and identify companies that are likely to be successful and profitable. This information can help businesses make informed decisions about mergers, acquisitions, and joint ventures.

Optimizing Marketing Campaigns

Tax data can also be used to optimize marketing campaigns by providing insights into the income levels and spending habits of different demographic groups. By analyzing tax data, businesses can target their marketing efforts more effectively and tailor their products and services to meet the needs of specific income groups. This can lead to increased sales and revenue.

Informed Investment Decisions

Investors can use tax data to make informed decisions about investment strategies. By understanding the tax implications of different investments, investors can minimize their tax liabilities and maximize their returns. For example, investors may choose to invest in tax-advantaged accounts, such as 401(k)s and IRAs, to reduce their tax burden.

Financial Planning

Tax data is invaluable for comprehensive financial planning. Understanding the impact of taxes on income and investments allows for strategic planning that minimizes tax liabilities and maximizes wealth accumulation. Financial advisors can use tax data to help clients make informed decisions about retirement planning, estate planning, and other financial goals.

Conclusion: The Significance of Understanding Tax Contributions

Understanding the tax contributions of different income groups is essential for informed policy debates, effective business strategies, and sound financial planning. The data reveal the progressive nature of the US federal income tax system and the significant role played by high-income earners. By leveraging tax data, businesses and investors can make informed decisions that optimize their financial outcomes.

At income-partners.net, we provide valuable insights and resources for businesses and investors looking to understand the tax landscape and make informed decisions. Our platform offers tools and information to help you identify strategic partnerships, optimize marketing campaigns, and make informed investment decisions. By understanding the tax contributions of different income groups, you can gain a competitive edge and achieve your financial goals. We strive to provide actionable insights and resources that empower our users to succeed.

Longitudinal trends of the top 1% income tax contributions

Longitudinal trends of the top 1% income tax contributions

Alt: This line graph depicts the shifting trends in the share of federal income taxes paid by the top 1% of taxpayers over time, showcasing an increasing contribution from this group.

Ready to take your business and investment strategies to the next level? Visit income-partners.net today to explore our resources and connect with potential partners. Discover how you can leverage tax insights to drive growth and success. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

Keywords: Tax contributions, high-income earners, strategic partnerships, marketing campaigns, tax rates, US federal income tax system, income inequality, financial planning.

LSI Keywords: Adjusted Gross Income (AGI), Internal Revenue Service (IRS), Tax Cuts and Jobs Act (TCJA).

FAQ: Understanding Tax Contributions by Top Earners

1. What percentage of income tax is paid by the top 1% in the US?

In 2021, the top 1% of taxpayers paid 45.8% of all federal income taxes in the United States. This figure underscores the substantial contribution of high-income earners to the federal tax revenue. This highlights the progressive nature of the tax system, where those with higher incomes pay a larger share.

2. How does the average income tax rate of the top 1% compare to other income groups?

The top 1% of taxpayers paid an average income tax rate of 25.9% in 2021, nearly eight times higher than the 3.3% average rate paid by the bottom half of taxpayers. This significant difference highlights the progressive structure of the US federal income tax system. The higher tax rate reflects the principle of ability to pay, where those with more income contribute a larger percentage.

3. What factors contribute to the high tax burden on the top 1%?

Several factors contribute to the high tax burden on the top 1%, including higher income levels, progressive tax rates, and capital gains realizations. High-income earners have substantial incomes that are taxed at higher rates, and they are more likely to realize significant capital gains, which also contribute to their tax liabilities.

4. How has the tax contribution of the top 1% changed over time?

Over the past several decades, the share of federal income taxes paid by the top 1% has generally increased. For example, the top 1%’s share of income taxes paid increased from 33.2% in 2001 to 45.8% in 2021. This trend reflects factors such as rising income inequality and changes in tax policies. Analyzing these shifts helps in understanding economic trends.

5. What was the adjusted gross income (AGI) threshold to be in the top 1% in 2021?

In 2021, the adjusted gross income (AGI) threshold for being in the top 1% was $682,577. This means that individuals or households with an AGI of $682,577 or more were considered to be in the top 1% of taxpayers. This income split point is essential for understanding economic stratification.

6. How did the American Rescue Plan Act (ARPA) impact tax contributions in 2021?

The American Rescue Plan Act (ARPA) provided tax relief to lower and middle-income groups through measures such as recovery rebates, expanded child tax credit (CTC), and earned income tax credit (EITC). These measures affected the distribution of tax burdens across income levels and provided financial support to those most affected by the pandemic. This resulted in shifts in the overall tax landscape.

7. How do capital gains realizations affect the tax contributions of high-income earners?

Capital gains realizations, the profits from the sale of assets like stocks and real estate, can significantly boost the incomes and tax liabilities of high-income earners. In 2021, capital gains realizations exceeded $2 trillion, reaching a 40-year high, which contributed to income growth and taxes paid for high-income groups. This illustrates the interplay between investment income and taxation.

8. How does the US federal income tax system compare to other countries in terms of progressivity?

The US federal income tax system is generally considered to be progressive, but its progressivity can vary depending on the specific tax policies in place. Compared to some other developed countries, the US may have a less progressive tax system, with lower top tax rates and fewer tax benefits for low-income individuals and families. This comparative perspective is crucial for policy evaluation.

9. How can businesses and investors use tax data to make informed decisions?

Businesses and investors can use tax data to identify strategic partnerships, optimize marketing campaigns, and make informed investment decisions. Understanding the tax landscape can provide a competitive edge and help optimize financial outcomes. For example, analyzing tax data can help businesses assess the financial stability of potential partners.

10. Where can I find more detailed data and analysis on tax contributions by income group?

More detailed data and analysis on tax contributions by income group can be found on the IRS website, the Tax Foundation website, and other reputable sources of tax information. These resources provide comprehensive data tables, reports, and analyses that can help you understand the tax landscape and make informed decisions. For additional insights, visit income-partners.net.