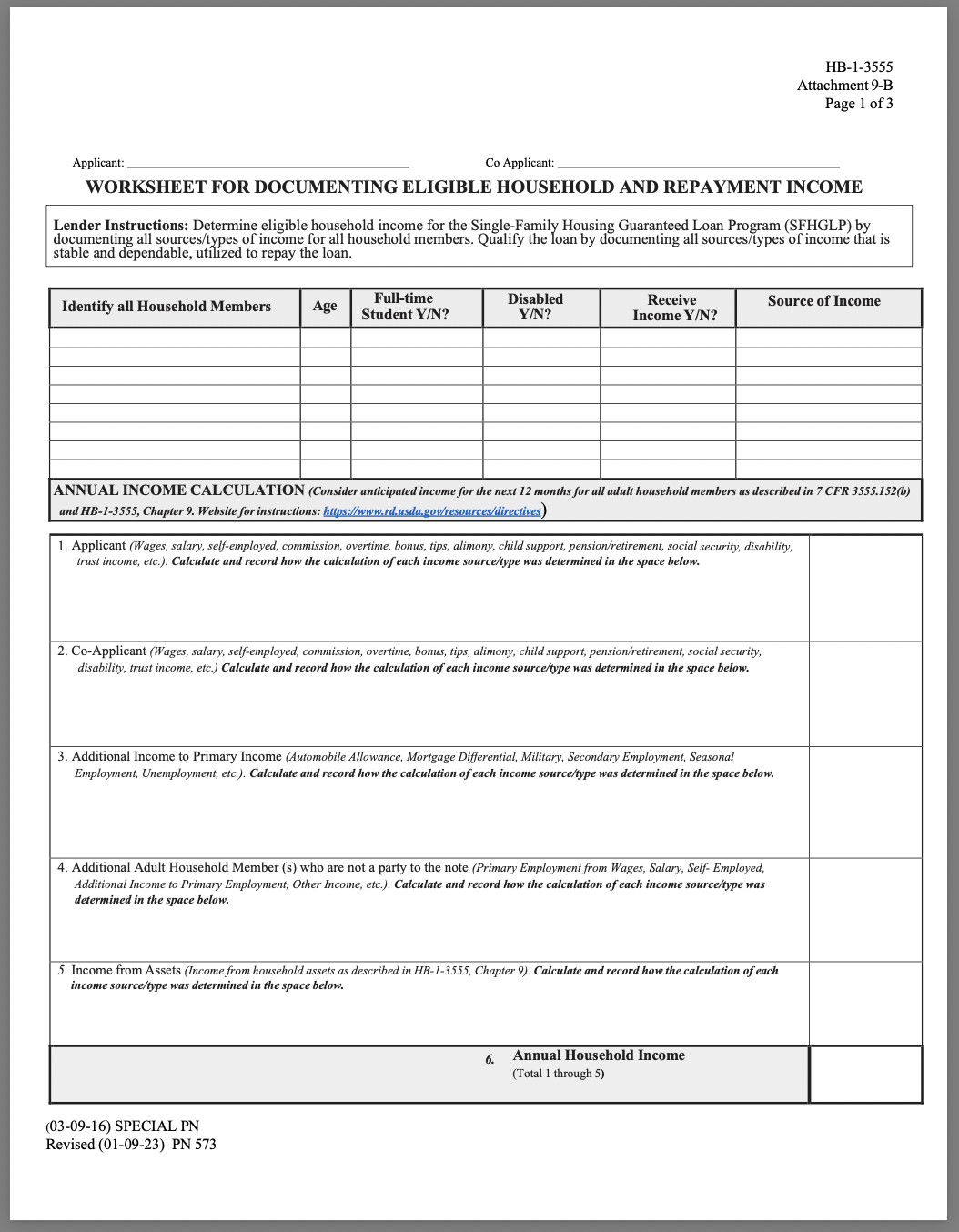

The USDA calculates household income for loan eligibility by considering the income of all adult household members, then subtracting applicable deductions to arrive at an adjusted annual income. At income-partners.net, we understand the intricacies of this process and can help you navigate it effectively, connecting you with strategic partners to enhance your financial success. Let’s delve into the specifics of how the USDA determines your eligibility, focusing on annual household income, adjusted annual income, and repayment income, all vital components for securing a USDA loan, ultimately leading to lucrative partnership opportunities and financial growth.

1. Understanding USDA Annual Household Income

The USDA loan program is designed to facilitate homeownership for low-to-moderate-income individuals in rural areas. USDA income requirements are in place to ensure that these loans remain accessible to those who need them most. Understanding these requirements is the first step toward determining your eligibility.

1.1. Defining Income Limits

While income restrictions for USDA loans can differ by region, the program does have some basic guidelines. For 2024, the USDA income limits are generally:

- Less than $112,450 for households of 1-4 people.

- Less than $148,450 for households of 5-8 people.

USDA annual income limits may be higher in areas where the cost of living exceeds the national average. It’s important to note that when determining USDA income eligibility, the income of each adult occupant (18 and older) is taken into consideration, regardless of whether they are co-borrowers. However, certain types of income are excluded from this calculation. These exclusions include:

- Section 8 or payments from other housing assistance programs

- Income earned by a full-time adult student that exceeds $480

- Income earned by a minor occupant

- One-time inheritance, capital gains, or insurance payouts

- Income earned by live-in aides

While determining annual household income is an important step, it isn’t the final determination of whether a borrower meets USDA income guidelines. Certain income streams may require more detailed consideration.

1.2. What Happens When Income is Hard to Document?

Documenting earnings from sources like Social Security or a salaried position can be relatively straightforward, but some situations are more complex. Here’s how the USDA handles a few common situations:

- Farm Income: Net operating income from a farm is generally added to the USDA annual income calculation. Farm expenditures cannot be used as a deduction in determining income. A net loss counts for $0 and can’t be used to offset other income types. However, deductions will factor into the adjusted annual income figure. Farmers can deduct property depreciation that occurs as a result of normal wear and tear.

- Business Income: Net operating income is considered when making a USDA income eligibility determination. A net loss counts for $0, but deductions for verifiable unreimbursed business expenses are taken into account for the purpose of determining adjusted annual income.

- Income-Producing Properties: Qualifying income from an income-producing property is calculated based on historical tax filing data. It’s essential to account for net operating income, and certain deductions may factor into the adjusted annual income.

- Overtime and Seasonal Employment: Individuals with fluctuating income on a seasonal or year-over-year basis should use historical data to calculate their USDA qualifying income. For example, a seasonal worker who earned $5,000 each fall for the last two years might project an additional $5,000 in seasonal earnings for the upcoming year. According to research from the University of Texas at Austin’s McCombs School of Business, analyzing historical data can provide a more accurate picture of income stability for seasonal workers.

- Assets: Income-generating assets held by any adult occupant can be evaluated to assess USDA qualifying income. Some common income-generating assets include:

- Investment accounts or properties

- Trust funds

- Proceeds from the sale of real estate

Cash and bank account balances may also be considered. Large deposits or account holdings that seem unusual compared to a borrower’s monthly earnings could signal income that is otherwise unaccounted for and may require additional verification.

Cash value for retirement accounts, life insurance policies, and personal property generally won’t be considered when calculating USDA qualifying income.

Homebuyers pursuing USDA loans must fulfill certain income requirements

Homebuyers pursuing USDA loans must fulfill certain income requirements

2. Calculating Adjusted Annual Income

Adjusted annual income is a critical figure that helps determine whether you meet the income restrictions for USDA loans. This calculation involves subtracting any applicable deductions from your annual income. Understanding these deductions can significantly impact your eligibility.

2.1. Qualified Deductions

There are five qualified deductions that can be used to reduce annual income:

- Dependent deduction: You can deduct $480 from annual income for every dependent who will use the new home as their primary residence.

- Child care expenses: You can deduct unreimbursed child care expenses for children 12 and under. Child care expenses qualify only when the care enables a family member to work outside the home.

- Elderly household deduction: You can deduct $400 from the annual income if a party to the note is at least 62 or is a person with a disability.

- Deduction for the care of household members with disabilities: You can deduct unreimbursed expenses for the care of a disabled person that exceeds 3% of the annual household income.

- Deduction for medical expenses: Elderly households can deduct unreimbursed medical expenses that exceed 3% of the annual household income when combined with any disability assistance expenses.

Your adjusted annual income cannot exceed 115% of the median income in your region. USDA income limits vary depending on the size of your family and location and are subject to change every year.

2.2. Understanding Regional Variations

It’s important to recognize that USDA income limits can vary significantly by region. Areas with a higher cost of living generally have higher income limits to accommodate the financial realities of those communities. To ensure accuracy, always consult the most current USDA income limits for your specific location. This information is readily available on the USDA website or through a trusted USDA lender.

For instance, a household in a high-cost area like Austin, TX, may have a higher income limit compared to a similar household in a more rural, low-cost area. This regional adjustment is crucial for ensuring that the USDA loan program remains accessible to those who need it most, regardless of where they live. Income-partners.net can provide you with the most up-to-date information and connect you with local experts who understand the nuances of your regional market.

3. Determining Repayment Income

Repayment income is a key factor that USDA lenders use to assess the creditworthiness of potential homebuyers. Lenders need to verify that a borrower has enough stable income to make on-time mortgage payments every month. This involves evaluating the borrower’s debt-to-income ratio (DTI), which compares their repayment income to their monthly expenditures.

3.1. Debt-To-Income Ratio (DTI)

The agency publishes a standard 41% DTI guideline for USDA loans. This means that borrowers are generally recommended to spend no more than 41% of their monthly income on debts, including the proposed monthly mortgage payment. However, there is some built-in flexibility.

When it comes to USDA loans and repayment income, lenders have the ultimate say in what it takes to qualify for financing. It is possible to get a USDA home loan with a DTI higher than 41%, assuming a borrower has qualifying credit and assets. According to a study by Harvard Business Review, lenders often consider compensating factors, such as a strong credit history and significant savings, to offset a higher DTI.

3.2. Calculating Repayment Income Sources

Repayment income includes stable, dependable income that is verifiable by a third party. Here’s how to calculate monthly income for some common repayment sources:

| Sources of Income | Calculation Method |

|---|---|

| Overtime/Bonuses | Minimum 2-year consecutive history. Take 24-month average based on net overtime/bonus income. |

| Commission | Minimum 2-year consecutive history. Take 24-month average based on net commissions. |

| Seasonal/Part-Time | Minimum 2-year history with verified continuance. Take 2-year average based on tax returns. |

| Tax Exempt | Since DTI calculations use taxed income, you can count 125% of any tax-exempt income. Multiply monthly amount by 1.25. |

| Military Pay/VA Benefits | Verified monthly base, housing, clothing, fight/hazard, reserve and disability pay is considered. Tax-exempt pay will be considered at 125% of the monthly amount. |

| Retirement/Social Security | Use an award letter to verify. Must continue for at least 3 years following the loan closing to be counted as repayment income. |

| Child Support/Alimony | Must continue for at least 3 years following the loan closing to be counted as repayment income. You must also verify the payments have been on-time for the previous 12 months. |

| Interest and Dividends | Minimum 2-year consecutive history. Take 24-month average based on net income from interest and dividends. |

| Rental Income | Net rental income, received for 24 months or more, can be considered for calculation of repayment income. |

3.3. Verifying Income Stability

Lenders place a significant emphasis on the stability and reliability of your income. To verify income, they typically require documentation such as:

- Pay stubs: Providing several months of pay stubs can demonstrate a consistent income pattern.

- W-2 forms: These forms summarize your annual earnings and taxes withheld.

- Tax returns: Tax returns provide a comprehensive overview of your income from all sources.

- Bank statements: Bank statements can help verify income deposits and overall financial stability.

- Award letters: For income sources like Social Security or retirement benefits, an award letter can confirm the amount and duration of the payments.

By thoroughly documenting your income sources, you can increase your chances of a smooth and successful loan approval process.

4. Common Mistakes to Avoid

Navigating the USDA loan income requirements can be complex, and it’s easy to make mistakes that could jeopardize your eligibility. Here are some common pitfalls to avoid:

- Miscalculating Household Income: One of the most common mistakes is failing to accurately calculate the total household income. Remember to include the income of all adult household members, even if they are not co-borrowers.

- Overlooking Deductions: Many borrowers miss out on valuable deductions that could significantly reduce their adjusted annual income. Be sure to carefully review all eligible deductions, such as dependent deductions, child care expenses, and deductions for elderly or disabled household members.

- Ignoring Regional Variations: USDA income limits vary by region, so it’s crucial to use the correct income limits for your specific location. Using outdated or incorrect income limits can lead to inaccurate eligibility assessments.

- Failing to Document Income Properly: Insufficient or incomplete income documentation is a common reason for loan denials. Make sure to gather all required documents, such as pay stubs, W-2 forms, tax returns, and bank statements, and ensure that they are accurate and up-to-date.

- Not Consulting with a USDA Lender: Many borrowers attempt to navigate the USDA loan process on their own, which can be overwhelming and confusing. Consulting with a knowledgeable USDA lender can provide valuable guidance and help you avoid costly mistakes.

By being aware of these common mistakes and taking steps to avoid them, you can increase your chances of a successful USDA loan application.

5. Expert Tips for Maximizing Your Chances

Securing a USDA loan can be a game-changer for aspiring homeowners in rural areas. Here are some expert tips to help you maximize your chances of approval:

- Improve Your Credit Score: A higher credit score can significantly improve your chances of loan approval and may also qualify you for a lower interest rate. Take steps to improve your credit score by paying bills on time, reducing debt, and correcting any errors on your credit report.

- Reduce Your Debt-To-Income Ratio: Lowering your DTI can make you a more attractive borrower to lenders. Focus on paying down debt and increasing your income to improve your DTI.

- Save for a Down Payment (Even Though It’s Not Required): While USDA loans do not require a down payment, having some savings can demonstrate financial responsibility and may increase your chances of approval.

- Choose the Right Property: USDA loans are only available for properties in eligible rural areas. Before you start your home search, make sure to verify that the properties you are interested in are located in USDA-eligible areas.

- Work with a Knowledgeable Real Estate Agent: A real estate agent who is experienced in USDA loans can provide valuable guidance and help you find properties that meet USDA requirements.

- Be Patient and Persistent: The USDA loan process can be complex and time-consuming, so it’s important to be patient and persistent. Don’t get discouraged if you encounter setbacks along the way. Keep working with your lender and real estate agent to overcome any challenges and achieve your homeownership goals.

According to Entrepreneur.com, building a strong relationship with your lender is crucial for navigating the complexities of the USDA loan process.

Homebuyers pursuing USDA loans must fulfill certain income requirements

6. How Income-Partners.Net Can Help

Navigating the complexities of USDA loan eligibility and income calculation can be daunting. At income-partners.net, we provide comprehensive resources and expert guidance to help you understand and meet the USDA’s requirements, paving the way for successful partnerships and financial growth.

6.1. Connecting You with Strategic Partners

We specialize in connecting individuals with strategic partners who can help them achieve their financial goals. Whether you’re looking to expand your business, invest in new opportunities, or simply improve your financial stability, our network of partners can provide the resources and support you need.

6.2. Providing Expert Guidance on USDA Loans

Our team of experts has extensive knowledge of USDA loan requirements and income calculation methods. We can help you:

- Determine your eligibility for a USDA loan

- Calculate your annual household income and adjusted annual income

- Identify eligible deductions to reduce your adjusted annual income

- Understand the income limits for your specific region

- Gather the necessary documentation to support your loan application

6.3. Offering Resources for Financial Growth

In addition to our USDA loan expertise, we offer a wide range of resources to help you achieve your financial goals. These resources include:

- Articles and guides on various financial topics

- Tools and calculators to help you manage your finances

- A directory of financial professionals and service providers

By leveraging our resources and expertise, you can take control of your financial future and achieve your dreams of homeownership and financial success.

7. The Benefits of USDA Loans for Homebuyers

USDA loans offer numerous advantages for eligible homebuyers, making them an attractive option for those looking to purchase property in rural areas. Understanding these benefits can help you make an informed decision about whether a USDA loan is right for you.

7.1. No Down Payment Required

One of the most significant benefits of USDA loans is that they do not require a down payment. This can be a major advantage for first-time homebuyers or those with limited savings, as it eliminates the need to accumulate a large sum of money upfront.

7.2. Low Interest Rates

USDA loans typically offer lower interest rates compared to conventional mortgages. This can save you a significant amount of money over the life of the loan, making homeownership more affordable.

7.3. Flexible Credit Requirements

USDA loans have more flexible credit requirements compared to conventional mortgages. This means that even if you have a less-than-perfect credit history, you may still be eligible for a USDA loan.

7.4. Guarantee Program

USDA loans are guaranteed by the U.S. Department of Agriculture, which reduces the risk for lenders. This guarantee allows lenders to offer more favorable terms and rates to borrowers.

7.5. Rural Development Focus

USDA loans are specifically designed to promote homeownership in rural areas. By providing access to affordable financing, USDA loans help to stimulate economic growth and improve the quality of life in rural communities.

8. Success Stories: Real-Life Examples of USDA Loans in Action

To illustrate the power and potential of USDA loans, let’s take a look at some real-life success stories:

- The Smith Family: The Smith family had always dreamed of owning a home, but they struggled to save enough money for a down payment. Thanks to a USDA loan, they were able to purchase their first home in a rural community without having to put any money down. The lower interest rate and flexible credit requirements made homeownership affordable for the Smith family.

- John and Mary: John and Mary were looking to start a small business in a rural area. They needed a loan to purchase property for their business, but they had limited credit history. A USDA loan helped them secure the financing they needed to purchase the property and launch their business.

- The Garcia Family: The Garcia family was living in a crowded apartment in the city and wanted to move to a more spacious home in the country. A USDA loan allowed them to purchase a larger home in a rural area with a lower interest rate than they could have obtained with a conventional mortgage. The USDA loan helped the Garcia family improve their quality of life and achieve their dream of owning a home in the country.

These success stories demonstrate the transformative impact that USDA loans can have on individuals and families in rural areas.

9. Frequently Asked Questions (FAQ) About USDA Income Calculation

1. How does the USDA define household income?

The USDA defines household income as the total income of all adult members (18 years or older) residing in the household, regardless of whether they are borrowers.

2. What types of income are included in the USDA household income calculation?

The USDA includes income from various sources, such as wages, salaries, self-employment, Social Security benefits, retirement income, and investment income.

3. Are there any types of income that are excluded from the USDA household income calculation?

Yes, certain types of income are excluded, such as Section 8 housing assistance payments, income earned by full-time students (up to a certain limit), and income earned by minor occupants.

4. What is adjusted annual income, and how is it calculated?

Adjusted annual income is calculated by subtracting certain deductions from the annual household income. These deductions may include dependent deductions, child care expenses, and deductions for elderly or disabled household members.

5. How do regional income limits affect USDA loan eligibility?

USDA income limits vary by region, with higher limits in areas with a higher cost of living. Borrowers must meet the income limits for their specific region to be eligible for a USDA loan.

6. What is repayment income, and why is it important?

Repayment income is the stable and dependable income that a borrower uses to make their monthly mortgage payments. Lenders use repayment income to assess a borrower’s ability to repay the loan.

7. How is debt-to-income ratio (DTI) used in the USDA loan process?

DTI compares a borrower’s monthly debt payments to their monthly income. Lenders use DTI to assess a borrower’s ability to manage their debt obligations.

8. What documentation is required to verify income for a USDA loan?

Borrowers typically need to provide documentation such as pay stubs, W-2 forms, tax returns, bank statements, and award letters (for income sources like Social Security).

9. Can self-employed individuals qualify for a USDA loan?

Yes, self-employed individuals can qualify for a USDA loan, but they will need to provide additional documentation to verify their income, such as tax returns and profit and loss statements.

10. Where can I find the most up-to-date USDA income limits for my region?

You can find the most up-to-date USDA income limits on the USDA website or by contacting a trusted USDA lender.

10. Take the Next Step Towards Homeownership and Financial Success

Understanding how the USDA calculates household income is crucial for determining your eligibility for a USDA loan. By taking the time to understand the income requirements and gather the necessary documentation, you can increase your chances of a successful loan application and achieve your dream of homeownership.

At income-partners.net, we are committed to helping you navigate the complexities of USDA loans and achieve your financial goals. Visit our website today to explore our resources, connect with strategic partners, and take the next step towards homeownership and financial success. Our comprehensive guides and expert support will empower you to make informed decisions and build a brighter future.

Ready to explore your options? Contact us at +1 (512) 471-3434 or visit our office at 1 University Station, Austin, TX 78712, United States. Let income-partners.net be your trusted partner on the path to financial prosperity.