Are you curious about How Much Percent Of Tax From Income Americans pay and how partnerships can help you manage your tax liability? At income-partners.net, we provide expert guidance on understanding income taxes and forming strategic alliances to optimize your financial strategies. We’ll delve into the details of the U.S. tax system, revealing how different income levels are taxed and exploring opportunities for business partnerships to create a more sustainable income revenue.

1. What Is The Average Income Tax Rate In The U.S.?

The average income tax rate in the U.S. varies depending on income level. In 2021, the average income tax rate was 14.9 percent. According to the latest data from the IRS, taxpayers reported over $14.7 trillion in adjusted gross income (AGI) and paid nearly $2.2 trillion in individual income taxes.

Understanding how the U.S. tax system affects individuals and businesses is essential for making informed financial decisions. At income-partners.net, we can help you navigate the tax landscape and find partnership opportunities to manage your tax liabilities effectively.

2. How Do Income Tax Rates Vary Across Different Income Groups?

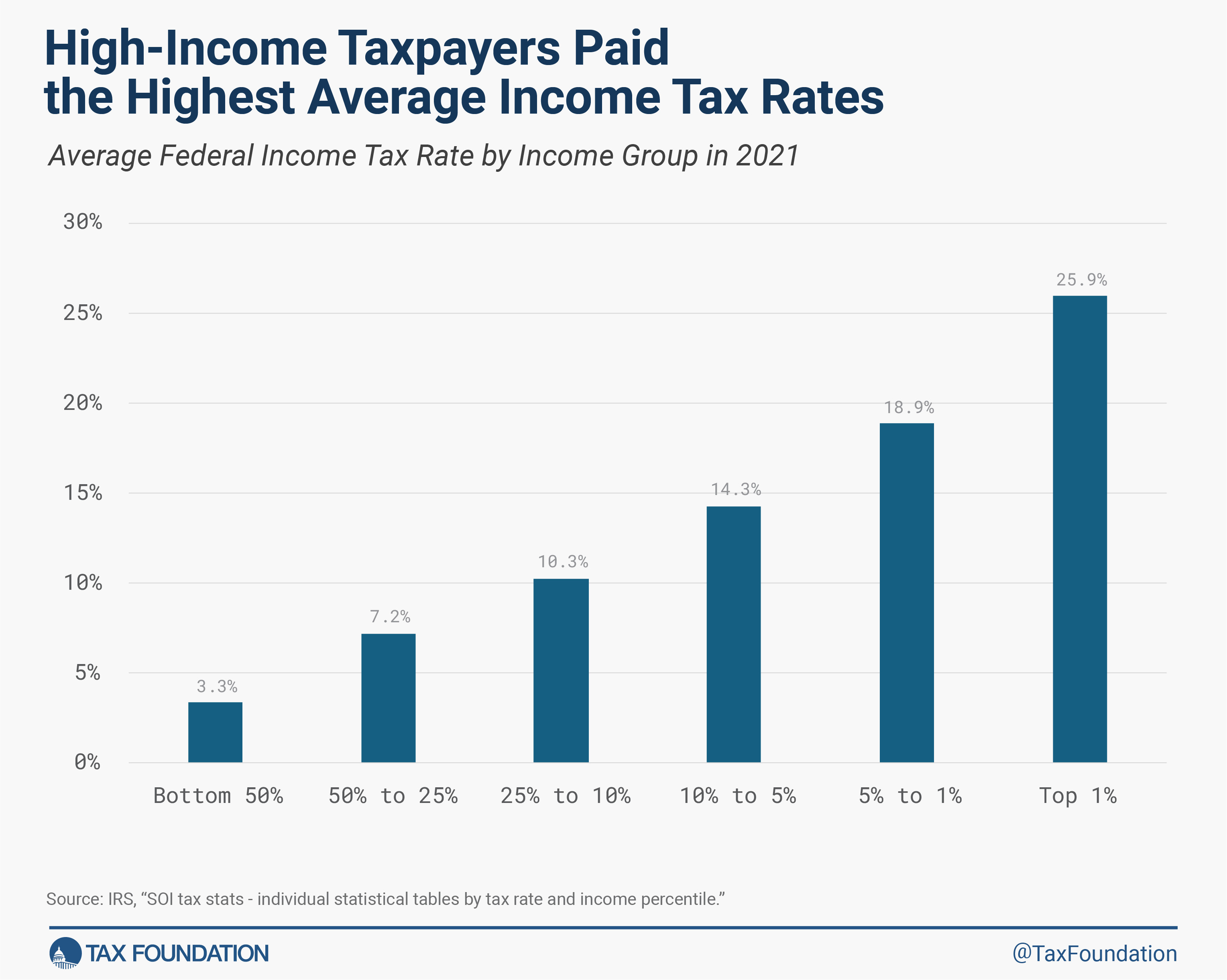

Income tax rates vary significantly across different income groups. In 2021, the top 1 percent of taxpayers paid an average rate of 25.9 percent, while the bottom half of taxpayers paid an average rate of 3.3 percent. The top 50 percent of all taxpayers paid 97.7 percent of all federal individual income taxes.

| Income Group | Average Tax Rate |

|---|---|

| Top 1% | 25.9% |

| Top 5% | 23.3% |

| Top 10% | 21.5% |

| Top 25% | 18.4% |

| Top 50% | 16.2% |

| Bottom 50% | 3.3% |

| All Taxpayers | 14.9% |

These figures illustrate the progressive nature of the U.S. tax system, where higher-income earners pay a larger percentage of their income in taxes.

Taxpayers with higher incomes pay much higher average income tax rates than taxpayers with lower incomes

Taxpayers with higher incomes pay much higher average income tax rates than taxpayers with lower incomes

Partnering with the right businesses can significantly impact your financial strategies and tax obligations. Visit income-partners.net to explore partnership opportunities tailored to your financial goals.

3. What Factors Influence Income Tax Rates In The U.S.?

Several factors influence income tax rates in the U.S., including income level, tax policy changes, and economic conditions. Pandemic-related tax items from the American Rescue Plan Act (ARPA) in 2021, such as recovery rebates and expanded child tax credits, also played a role.

Understanding these factors can help businesses and individuals anticipate changes in their tax liabilities. income-partners.net offers insights into economic trends and policy changes that could affect your tax planning.

4. How Does The Tax Cuts And Jobs Act (TCJA) Affect Average Tax Rates?

The Tax Cuts and Jobs Act (TCJA), enacted in 2017, made significant temporary changes to the individual income tax code. It lowered tax rates, widened brackets, and increased the standard deduction and child tax credit. These changes generally lowered tax burdens across all income levels.

In 2021, average tax rates remained lower than in 2017, prior to the TCJA, across all income groups. Tax relief in the form of expanded tax credits also affected average tax rates for middle- and lower-income taxpayers.

The TCJA’s impact on tax rates highlights the importance of staying informed about tax law changes and their potential effects. Visit income-partners.net to discover strategies for adapting to evolving tax policies and maximizing your financial outcomes through strategic alliances.

5. What Role Do High-Income Taxpayers Play In The Federal Income Tax System?

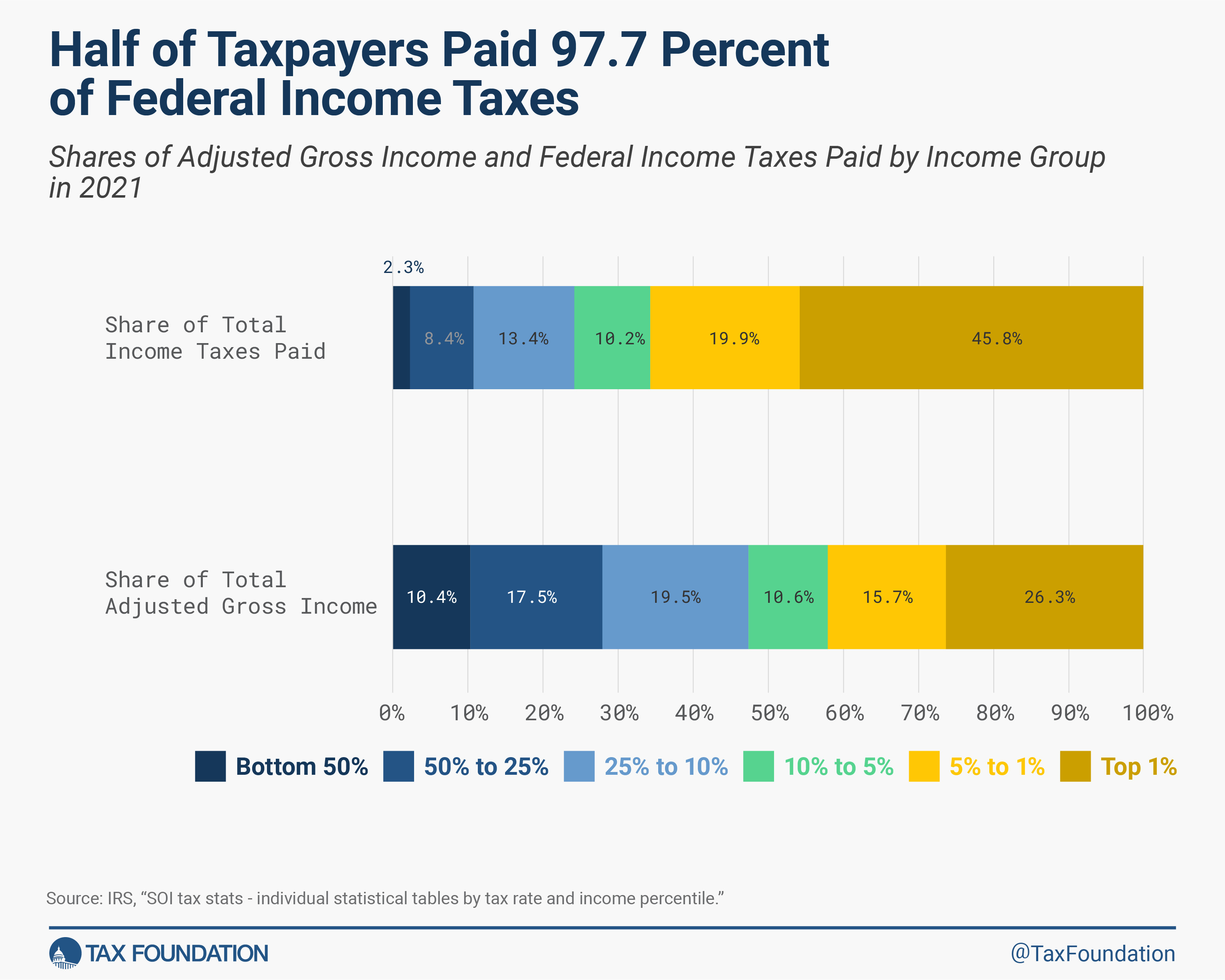

High-income taxpayers play a significant role in the federal income tax system. In 2021, the top 1 percent of taxpayers earned 26.3 percent of total AGI and paid 45.8 percent of all federal income taxes. The top 50 percent of all taxpayers paid 97.7 percent of all federal individual income taxes, while the bottom 50 percent paid the remaining 2.3 percent.

| Category | Share of Total AGI | Share of Total Income Taxes Paid |

|---|---|---|

| Top 1% | 26.3% | 45.8% |

| Bottom 50% | 10.4% | 2.3% |

These figures underscore the progressive nature of the tax system and the substantial contribution of high-income earners.

To optimize your financial strategies and manage your tax liabilities effectively, consider exploring partnership opportunities at income-partners.net.

6. How Did Pandemic-Related Relief Programs Impact Income Taxes?

Pandemic-related relief programs, such as those included in the American Rescue Plan Act (ARPA), significantly impacted income taxes. These programs provided recovery rebates, expanded premium tax credits, increased the child tax credit (CTC), and enhanced the earned income tax credit (EITC).

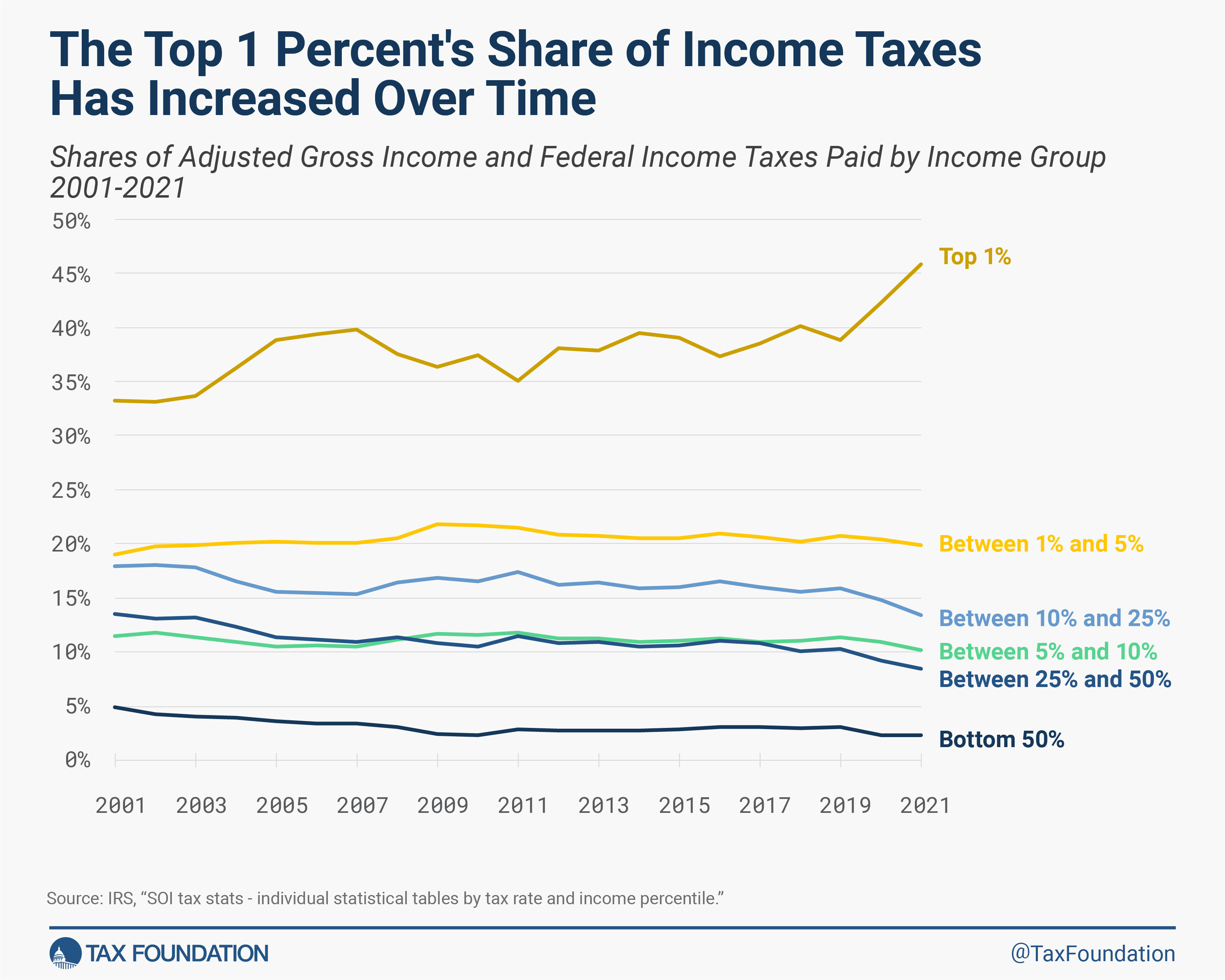

From 2020 to 2021, AGI grew across all income groups, but faster among higher-income groups due to a significant increase in capital gains realizations. These factors, combined with tax credit expansions for middle- and lower-income groups, resulted in a larger share of income reported and taxes paid at the top and a higher average income tax rate overall.

The pandemic relief measures underscore the importance of adapting to economic changes and leveraging available tax benefits. At income-partners.net, we provide up-to-date insights on policy changes and strategies to optimize your financial planning during evolving economic conditions.

7. What Is Adjusted Gross Income (AGI) And Why Is It Important?

Adjusted Gross Income (AGI) is an individual’s total gross income minus specific deductions. Gross income includes wages, salaries, investment income, and other forms of earnings. Deductions can include contributions to retirement accounts, student loan interest payments, and other eligible expenses.

AGI is important because it is used to determine eligibility for various tax credits and deductions, as well as to calculate your taxable income. A lower AGI can result in a lower tax liability.

Understanding AGI and how to optimize it is crucial for effective tax planning. Visit income-partners.net to learn more about strategies for managing your AGI and exploring partnership opportunities that can enhance your financial outcomes.

8. How Do Capital Gains Realizations Affect Income Taxes?

Capital gains realizations occur when an asset, such as stocks or real estate, is sold for a profit. The profit is subject to capital gains taxes, which can vary depending on the holding period (short-term or long-term) and the taxpayer’s income level.

In 2021, capital gains realizations exceeded $2 trillion, reaching a 40-year high and driving income growth and taxes paid for high-income groups. Higher growth at higher income levels, combined with significant expansions of tax credits for middle- and lower-income groups, resulted in a larger share of income reported and taxes paid at the top and a higher average income tax rate overall.

Capital gains realizations can significantly impact your overall tax liability. income-partners.net offers insights into managing capital gains taxes and exploring partnership opportunities to optimize your investment strategies.

9. What Are Some Common Tax Credits And Deductions Available To Taxpayers?

Tax credits and deductions can reduce your tax liability by either lowering your taxable income (deductions) or providing a dollar-for-dollar reduction in your tax bill (credits). Some common tax credits and deductions include:

- Child Tax Credit (CTC): A credit for each qualifying child.

- Earned Income Tax Credit (EITC): A credit for low- to moderate-income working individuals and families.

- Standard Deduction: A set amount that reduces your taxable income.

- Itemized Deductions: Deductions for specific expenses, such as medical expenses, state and local taxes (SALT), and charitable contributions.

- Retirement Contributions: Deductions for contributions to retirement accounts, such as 401(k)s and IRAs.

Understanding and utilizing these credits and deductions can significantly lower your tax burden. At income-partners.net, we can help you identify applicable credits and deductions and explore partnership opportunities that can further optimize your tax planning.

10. How Can Strategic Business Partnerships Help Manage Income Taxes?

Strategic business partnerships can offer numerous benefits for managing income taxes, including:

- Resource Sharing: Partners can pool resources to reduce individual expenses and increase efficiency.

- Tax Planning: Partners can collaborate on tax planning strategies to minimize their overall tax liabilities.

- Diversification: Partners can diversify their income streams and reduce risk.

- Economies of Scale: Partners can achieve economies of scale, lowering costs and increasing profitability.

- Access to Expertise: Partners can gain access to specialized knowledge and skills.

By forming strategic alliances, businesses and individuals can optimize their financial strategies and manage their tax obligations more effectively. Visit income-partners.net to explore partnership opportunities tailored to your financial goals and tax planning needs.

Half of taxpayers pay over 97 percent of federal income taxes, according to the latest federal income tax data

Half of taxpayers pay over 97 percent of federal income taxes, according to the latest federal income tax data

11. What Are The Key Takeaways From The IRS Data On Income Taxes?

The IRS data on income taxes reveals several key trends:

- Progressive Tax System: High-income taxpayers pay a larger percentage of their income in taxes.

- Impact of Tax Policy: Changes in tax laws, such as the TCJA, can significantly affect average tax rates.

- Economic Factors: Economic conditions, such as capital gains realizations, influence income growth and tax liabilities.

- Relief Programs: Pandemic-related relief programs had a substantial impact on income taxes.

- Importance of Tax Planning: Effective tax planning is crucial for managing tax obligations and optimizing financial outcomes.

Staying informed about these trends and understanding their implications can help businesses and individuals make informed financial decisions. income-partners.net provides insights into these key takeaways and offers strategies for navigating the evolving tax landscape.

12. How Can I Stay Informed About Changes In Tax Policies?

Staying informed about changes in tax policies is essential for effective tax planning. Here are several ways to stay up-to-date:

- Follow Reputable News Sources: Stay informed about tax policy changes by following reputable news sources, such as The Wall Street Journal, Bloomberg, and Forbes.

- Subscribe to Tax Newsletters: Subscribe to tax newsletters from organizations like the Tax Foundation and professional services firms.

- Consult with a Tax Professional: Work with a qualified tax professional who can provide personalized advice and keep you informed about relevant tax law changes.

- Monitor IRS Updates: Regularly check the IRS website for updates on tax laws, regulations, and guidance.

- Engage with Industry Associations: Participate in industry associations that provide updates on tax policy changes affecting your business or sector.

income-partners.net also offers resources and insights to help you stay informed about changes in tax policies and their potential effects.

13. What Is The Role Of Tax Professionals In Income Tax Planning?

Tax professionals play a crucial role in income tax planning by providing expert advice, preparing tax returns, and helping individuals and businesses navigate the complex tax landscape. They can:

- Provide Expert Advice: Tax professionals have in-depth knowledge of tax laws and regulations and can provide personalized advice tailored to your specific circumstances.

- Prepare Tax Returns: They can accurately prepare and file your tax returns, ensuring compliance with all applicable laws.

- Identify Tax-Saving Opportunities: They can identify potential tax credits, deductions, and other tax-saving opportunities that you may not be aware of.

- Represent You Before the IRS: In the event of an audit or other tax dispute, they can represent you before the IRS and advocate on your behalf.

- Offer Proactive Tax Planning: They can help you develop proactive tax planning strategies to minimize your tax liabilities and optimize your financial outcomes.

Engaging a tax professional can be a valuable investment for managing your income taxes effectively. At income-partners.net, we can connect you with qualified tax professionals and explore partnership opportunities that can further enhance your tax planning strategies.

14. How Can I Use Tax Planning To Increase My Income?

Effective tax planning can help you increase your income by reducing your tax liabilities and optimizing your financial strategies. Some strategies include:

- Maximizing Deductions: Take advantage of all eligible deductions to reduce your taxable income.

- Utilizing Tax Credits: Claim all applicable tax credits to lower your tax bill.

- Investing in Tax-Advantaged Accounts: Contribute to retirement accounts and other tax-advantaged accounts to defer or eliminate taxes on your investment earnings.

- Timing Income and Expenses: Strategically time your income and expenses to minimize your tax liabilities.

- Forming Strategic Partnerships: Collaborate with other businesses or individuals to share resources, reduce expenses, and optimize tax planning strategies.

By implementing these strategies, you can reduce your tax burden and increase your overall income. income-partners.net offers resources and insights to help you develop effective tax planning strategies and explore partnership opportunities that can enhance your financial outcomes.

15. What Are Some Common Mistakes To Avoid When Filing Income Taxes?

Filing income taxes can be complex, and it’s easy to make mistakes. Some common mistakes to avoid include:

- Missing Deadlines: Failing to file your tax return or pay your taxes by the due date can result in penalties and interest charges.

- Incorrect Information: Providing inaccurate or incomplete information on your tax return can lead to errors and delays.

- Failing to Claim Eligible Credits and Deductions: Overlooking potential tax credits and deductions can result in a higher tax liability.

- Not Keeping Adequate Records: Failing to maintain proper records of your income, expenses, and other relevant information can make it difficult to prepare your tax return accurately.

- Ignoring Changes in Tax Laws: Not staying informed about changes in tax laws can lead to errors and missed opportunities.

Avoiding these common mistakes can help you file your income taxes accurately and efficiently. income-partners.net offers resources and insights to help you navigate the tax filing process and avoid potential pitfalls.

16. How Do State And Local Taxes Affect Overall Tax Burden?

State and local taxes can significantly affect the overall tax burden on individuals and businesses. In addition to federal income taxes, taxpayers may also be subject to state income taxes, property taxes, sales taxes, and other local taxes.

The impact of state and local taxes can vary depending on the jurisdiction and the taxpayer’s specific circumstances. Some states have higher income tax rates than others, while others rely more heavily on property or sales taxes.

Understanding how state and local taxes affect your overall tax burden is essential for effective financial planning. income-partners.net offers resources and insights to help you navigate the complexities of state and local taxes and explore partnership opportunities that can optimize your tax strategies across different jurisdictions.

17. What Are The Tax Implications Of Owning A Small Business?

Owning a small business can have significant tax implications. Small business owners may be subject to self-employment taxes, as well as income taxes on their business profits. They may also be eligible for various tax deductions and credits, such as the qualified business income (QBI) deduction.

The tax implications of owning a small business can vary depending on the business structure (e.g., sole proprietorship, partnership, S corporation, C corporation) and other factors. Effective tax planning is crucial for managing tax obligations and maximizing profitability.

income-partners.net offers resources and insights to help small business owners navigate the tax landscape and explore partnership opportunities that can enhance their financial outcomes.

18. How Does The IRS Define Taxable Income?

The IRS defines taxable income as adjusted gross income (AGI) less itemized deductions or the standard deduction. Taxable income is the amount of income subject to income tax.

Calculating taxable income is a crucial step in preparing your tax return. It involves determining your AGI, subtracting any eligible deductions, and applying the appropriate tax rates to arrive at your tax liability.

Understanding how the IRS defines taxable income is essential for accurate tax planning and compliance. income-partners.net offers resources and insights to help you navigate the process of calculating your taxable income and optimizing your tax strategies.

19. What Are The Long-Term Trends In Federal Income Tax Rates And Shares?

Long-term trends in federal income tax rates and shares reveal several key patterns:

- Progressive Tax System: The U.S. federal income tax system has generally been progressive, with higher-income taxpayers paying a larger percentage of their income in taxes.

- Shifting Tax Burden: The share of federal income taxes paid by the top 1 percent of taxpayers has increased over time, while the share paid by the bottom 50 percent has decreased.

- Impact of Tax Policy Changes: Changes in tax laws, such as the Tax Cuts and Jobs Act (TCJA), can significantly affect average tax rates and shares.

- Economic Factors: Economic conditions, such as capital gains realizations and income inequality, influence the distribution of income and taxes paid.

Understanding these long-term trends can help businesses and individuals anticipate future changes in the tax landscape and plan accordingly. income-partners.net offers insights into these trends and strategies for adapting to the evolving tax environment.

The top 1 percent of taxpayers pay more in taxes over time20. How Can Partnering With Income-Partners.Net Help Me With Income Tax Planning?

The top 1 percent of taxpayers pay more in taxes over time20. How Can Partnering With Income-Partners.Net Help Me With Income Tax Planning?

Partnering with income-partners.net can provide numerous benefits for income tax planning, including:

- Expert Insights: Access to expert insights and resources on tax laws, regulations, and strategies.

- Partnership Opportunities: Connection with potential business partners to share resources, reduce expenses, and optimize tax planning.

- Personalized Guidance: Tailored advice and support to help you navigate the complexities of income tax planning.

- Up-to-Date Information: Stay informed about changes in tax policies and economic conditions that could affect your tax liabilities.

- Enhanced Financial Outcomes: Optimize your financial strategies and increase your income by reducing your tax burden.

By partnering with income-partners.net, you can gain a competitive edge in managing your income taxes effectively. Visit our website at income-partners.net to explore partnership opportunities and discover how we can help you achieve your financial goals.

These insights aim to inform and empower you. The information provided here is for informational purposes only and does not constitute financial or tax advice. Always consult with a qualified professional for personalized advice based on your specific circumstances.

FAQ: Understanding Income Taxes and Strategic Partnerships

1. What is the primary goal of income tax planning?

The primary goal is to minimize your tax liability while remaining compliant with tax laws. Effective planning can lead to significant savings.

2. How do tax deductions help reduce my taxable income?

Tax deductions lower the amount of income that is subject to tax, which in turn reduces your overall tax liability.

3. What is the difference between tax credits and tax deductions?

Tax credits directly reduce the amount of tax you owe, while tax deductions reduce your taxable income. Tax credits generally offer a greater benefit.

4. Why is Adjusted Gross Income (AGI) an important figure in tax planning?

AGI is used to determine eligibility for various tax credits and deductions, as well as to calculate your taxable income.

5. How does strategic business partnering contribute to better tax management?

Strategic partnerships allow for resource sharing and collaborative tax planning, which can lead to optimized tax strategies and reduced liabilities.

6. Can capital gains realizations significantly impact my income taxes?

Yes, capital gains realizations can substantially increase your tax liability, especially for high-income earners.

7. What role do tax professionals play in income tax planning?

Tax professionals offer expert advice, ensure compliance, and identify tax-saving opportunities, making them invaluable for effective tax management.

8. How can I stay updated on the latest changes in tax policies?

Following reputable news sources, subscribing to tax newsletters, and consulting with a tax professional are great ways to stay informed.

9. What are the potential risks of not engaging in proper tax planning?

Without proper tax planning, you risk overpaying your taxes, missing out on valuable deductions and credits, and facing penalties for non-compliance.

10. What types of resources does income-partners.net offer for income tax planning?

income-partners.net provides expert insights, partnership opportunities, personalized guidance, and up-to-date information to enhance your tax planning efforts.

At income-partners.net, we provide expert guidance on understanding income taxes and forming strategic alliances to optimize your financial strategies. Let us help you navigate the tax landscape and explore opportunities for business partnerships to create a more sustainable income revenue. Contact us at Address: 1 University Station, Austin, TX 78712, United States, Phone: +1 (512) 471-3434 or visit our Website: income-partners.net today to get started.