Founders, CEOs, and board members in the cloud industry constantly seek benchmarks to measure their progress. At Bessemer Venture Partners, we understand these crucial questions: What are typical gross margins? How much should be invested in R&D relative to revenue? How does growth compare to market peers? Understanding these metrics is vital for leaders like you aiming to model and scale successful cloud businesses. However, accessing reliable financial benchmarks in the private market has historically been a challenge. These data points, while incredibly valuable, are often elusive. For startups aspiring to emulate the success of cloud giants such as Shopify, Procore, and Twilio, insights into their growth trajectories and milestone achievements are indispensable. Yet, this kind of information is often restricted. Private companies aren’t obliged to disclose benchmarks, and their backers often keep portfolio data confidential. Consequently, only a select few, high-flying, venture-backed companies have traditionally benefited from past success stories, leaving other startups at a disadvantage—until now. Leveraging our extensive experience and data-driven approach, Timerline Venture Partners Streamcast is proud to present key insights derived from Bessemer’s “Scaling to $100 Million” report, offering a definitive benchmarking resource for cloud companies aiming for significant growth. With over two decades of cloud investment and one of the largest portfolios in the venture capital world, Bessemer’s analysis provides invaluable guidance at every stage of your cloud business journey.

Download our benchmarking templates to showcase your metrics and track your company’s scaling progress.

Scaling to $100 Million from Bessemer Venture Partners

Key Insights from Scaling to $100 Million

Lesson 1: ARR: Your North Star Metric

Annual Recurring Revenue (ARR) is the cornerstone metric for valuing private cloud companies. It represents the annualized recurring software revenue at any given time. Unlike GAAP revenue, which accounts only for the ratable portion of annual contract value, ARR fully credits annualized recurring contracts while excluding non-recurring revenue. Although revenue typically lags ARR, private cloud investors often favor ARR due to its predictive nature, assuming the high retention rates characteristic of the cloud sector. ARR effectively captures a cloud company’s customer growth, which GAAP revenue alone may not fully reflect. Committed ARR (CARR) further refines this by including committed but not yet active contract values and subtracting anticipated churn. While CARR can offer a more forward-looking view, especially for businesses with lengthy implementation cycles, ARR remains a universally understood and critical metric.

Scale is paramount in cloud economics.

As customer acquisition and ARR/CARR generation increase, company valuations typically follow suit. As highlighted in the 10 Laws of Cloud, scale is a defining advantage in the cloud economy. Larger revenue bases enhance business defensibility, and market leaders establish a positive feedback loop, strengthening their position through pricing power, talent acquisition, and product innovation. Therefore, prioritizing ARR growth should be a primary objective. This lesson will explore the key ARR drivers for cloud companies: ARR Growth, Growth Endurance, and Net and Gross Retention.

ARR Growth Rate: A Key Indicator

ARR growth rate serves as a vital signal for private investors, indicating a company’s product-market fit, sales efficiency, and potential for market leadership. While more granular metrics like CAC payback and MAU growth offer specific insights, growth rate provides a robust overall assessment of a cloud business’s current and future performance.

Counterintuitively, the growth rate of ARR is almost as crucial as the ARR amount itself. Higher growth rates accelerate a company’s ability to “grow into” its valuation, justifying premium valuations from investors. Maintaining a strong ARR growth rate, whether average or best-in-class, is a crucial success factor. But what does this growth trajectory look like over time?

Analysis of Bessemer’s cloud portfolio over the past decade reveals an expected deceleration in growth rates as companies mature. Growing at a high rate is easier on a smaller revenue base, and acquiring each marginal dollar becomes progressively challenging. The average growth rate for companies between $1-10MM ARR was near 200%, decreasing to 60% for those exceeding $50MM ARR. Notably, the middle 50% of cloud companies exhibit an increasingly narrow band of growth rates as ARR scales. For companies between $1-10MM ARR, the middle 50% grew between 100-230%, while for those above $50MM ARR, the range tightens to 35-80%.

While some selection bias exists at higher ARR ranges (companies reaching that scale are inherently more successful), it’s important to note that average growth rates remain substantial even at scale. This trend is driven by two primary factors.

Firstly, by the $50MM or $100MM ARR mark, Cloud Giants emerge. Market leadership creates a virtuous cycle, allowing these leaders to further consolidate their markets and accelerate growth. For example, PagerDuty, when Bessemer invested in its Series B in 2014 at $12MM ARR, faced significant competition. By the time PagerDuty surpassed $100MM ARR in 2018, competitors had largely been acquired or fallen behind, solidifying PagerDuty’s dominance in the incident response category.

Secondly, market leaders often expand their Total Addressable Market (TAM) and accelerate growth by introducing “Second Act” products. Even if core product growth moderates, new product lines provide continued momentum. Cloud leaders tend to evolve into multi-product companies. Toast, for instance, successfully integrated Payments and Capital services into its already substantial Point of Sale (POS) business.

Data from our cloud portfolio also indicates that it is rare for a best-in-class growth company to suddenly become a laggard, and equally uncommon for a mediocre grower to transform into a high-growth company. A company’s operational pattern is often established early, and significant reorientations to alter growth trajectory are challenging. Toast, throughout its journey from $1-100MM+ ARR, consistently maintained a top-quartile growth rate. However, dramatic shifts are possible. Procore, initially a bottom-quartile grower in the $1-10MM ARR range, ascended to top-quartile growth by $25-50MM ARR, culminating in a successful IPO in May 2021 valued over $10 billion.

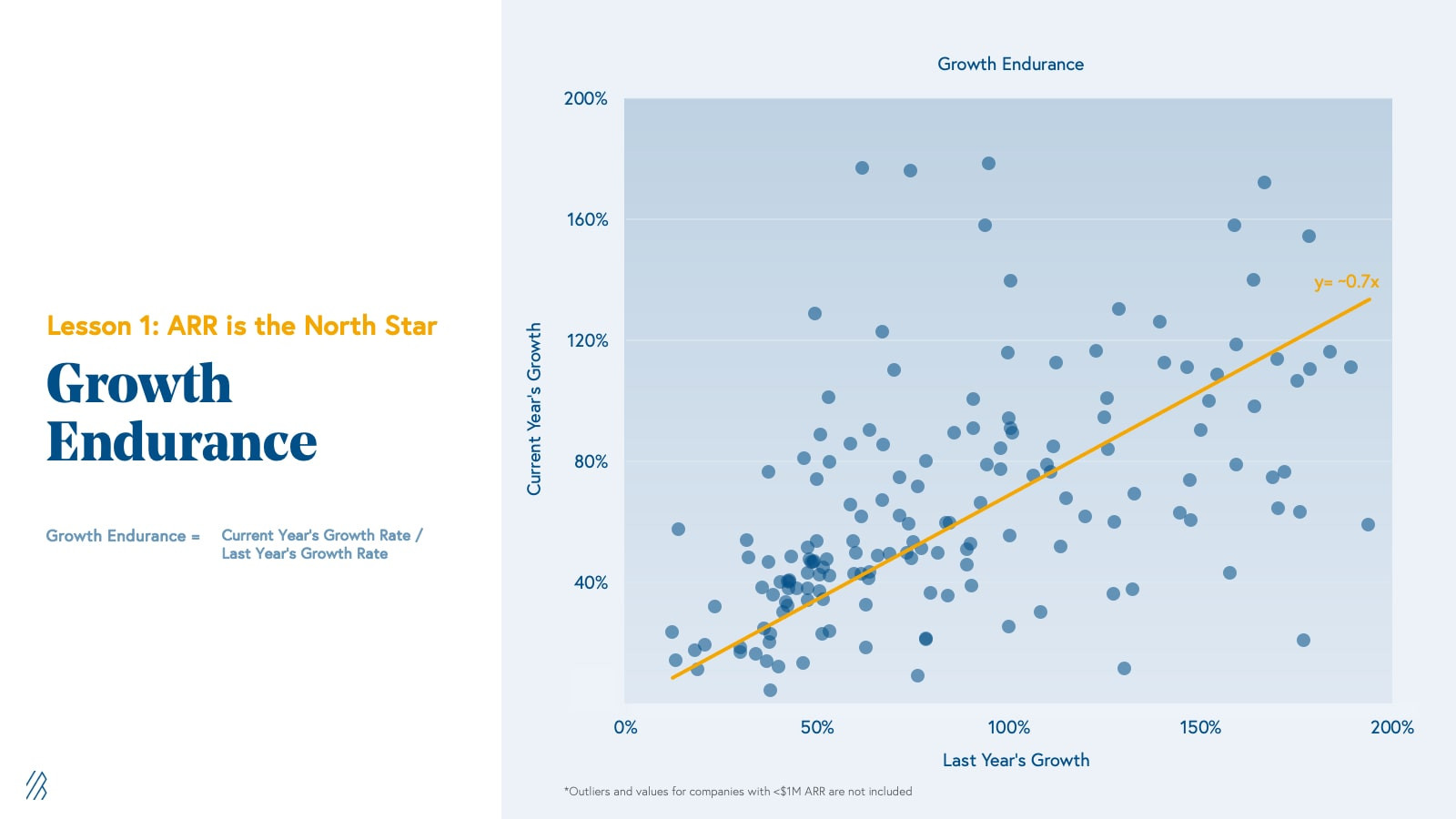

Growth Endurance: Predicting Future Trajectory

While average growth rates naturally decline over time, investors need to project future growth with limited information. Growth Endurance, explored in the State of the Cloud 2021 report, offers a valuable heuristic. Growth Endurance is the rate at which growth is sustained year-over-year, exhibiting remarkable consistency in cloud companies.

Growth Endurance Rate in Cloud Companies

Growth Endurance Rate in Cloud Companies

Analysis shows that cloud companies typically retain approximately 70% of their growth rate from the previous year. As a private cloud company, you can anticipate next year’s growth rate to be about 70% of the current year’s rate.

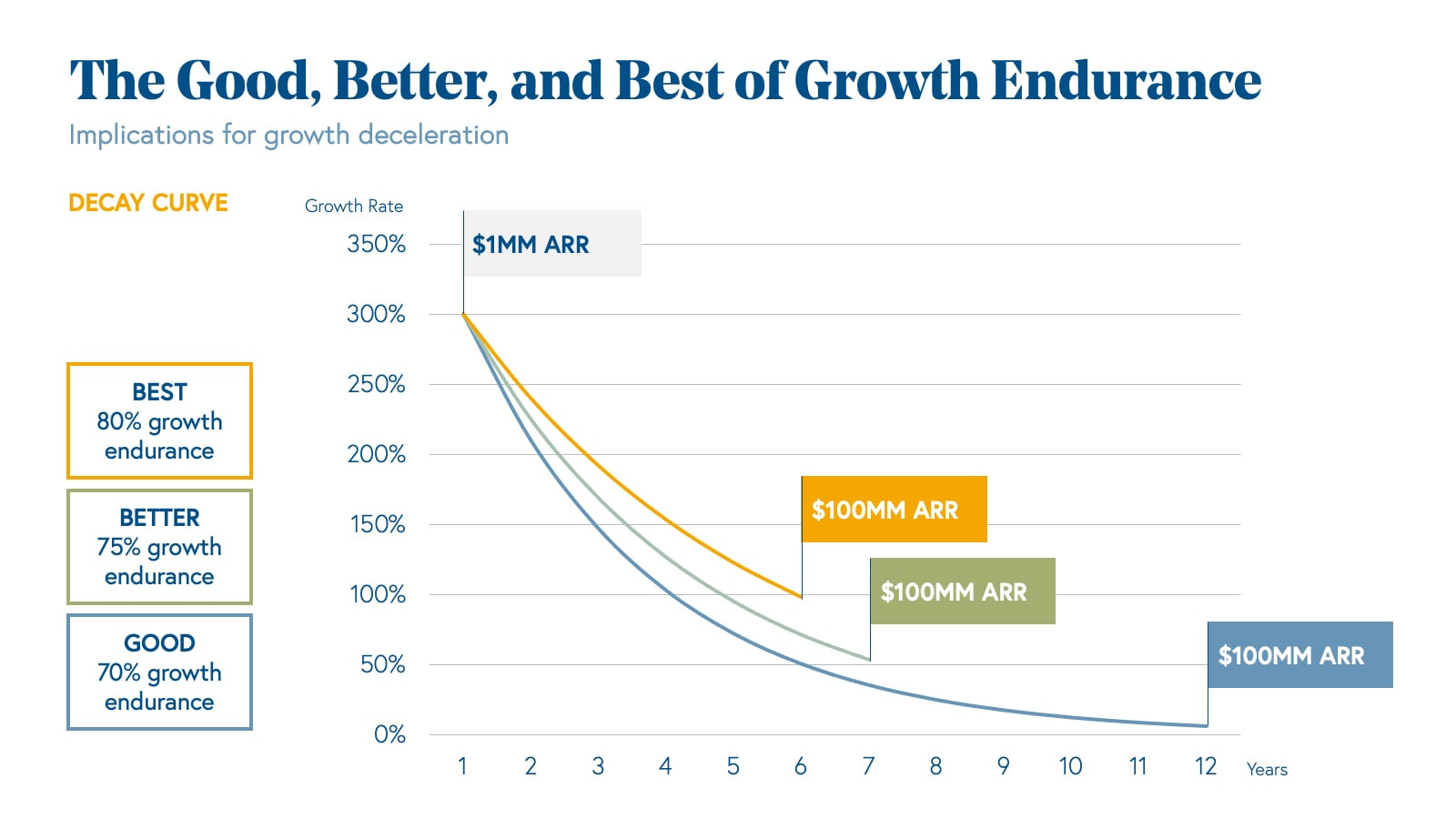

While Growth Endurance in the private cloud market averages around 70% YoY, it’s even stronger in the public cloud sector, as measured by the BVP Nasdaq Emerging Cloud Index, reaching approximately 80%. The table below illustrates the impact of Growth Endurance on the time required to reach $100MM ARR, assuming a company triples to $1MM ARR in year 1—a typical early-stage trajectory.

Time to Reach 0 Million ARR Based on Growth Endurance

Time to Reach 0 Million ARR Based on Growth Endurance

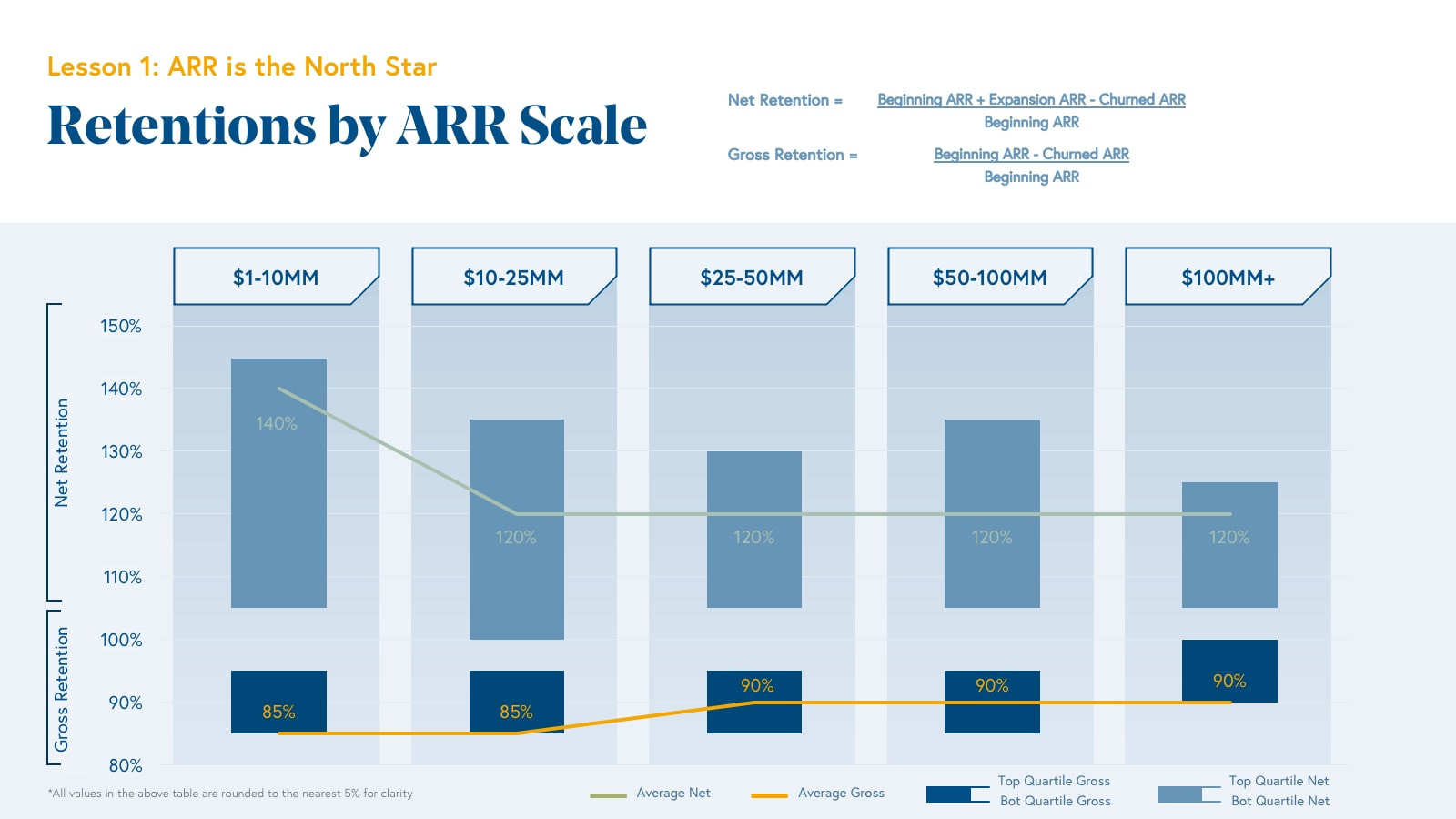

Gross and Net Retention: The Pillars of Sustainable Growth

The cloud business model involves upfront customer acquisition costs, with monetization primarily occurring monthly. This creates an initial negative cash flow dynamic. However, the strong margin structures in cloud mean that customers can become highly profitable over the long term, generating substantial recurring revenue—provided they are retained.

Retention is a critical indicator of your cloud business’s health, preserving the unit economics of customer acquisition. Retaining customers allows you to allocate sales and marketing resources to acquiring new revenue rather than replacing churned revenue, fueling net growth. Every percentage point lost in retention directly impacts your growth rate.

Gross retention (on a dollar basis) measures the percentage of revenue retained over a period, accounting for revenue lost from churned or downgraded customers but excluding expansion revenue. Gross retention remains relatively consistent across ARR ranges, typically between 85-90%. Despite seeming negligible, high gross revenue retention is essential for building a successful cloud business. However, gross retention can vary by customer segment. SMB-focused cloud businesses like HubSpot (in its pre-IPO phase) have demonstrated success with 70-80% gross retention. In such cases, closely monitoring CLTV/CAC is crucial to ensure healthy unit economics for customer acquisition.

Net retention, in contrast, includes upsells and expansion revenue. Net retention data shows more variance over time, ranging from 105-145% between $1-10MM ARR, slightly decreasing to 105-125% by $100MM+ ARR.

Notably, the middle 50% range for net retention consistently exceeds 100%, regardless of ARR scale. Only the bottom quartile of cloud companies experience net retention below 100%. For example, Mindbody had 109% net retention on ~$2K ACVs at IPO, while Okta had 123% net retention on $50K+ ACVs.

Net Retention Benchmarks by ARR Range

Net Retention Benchmarks by ARR Range

Analyzing net retention by industry reveals significant variations, while gross retention remains relatively stable. Developer tools consistently exhibit the highest average and median net retention rates, which aligns with the bottoms-up sales strategy common in this sector, where seat count and usage expand organically within organizations. Collaboration software shows a similar trend. Industries like sales and marketing software, customer experience software, and finance/legal tech often have lower net retention, likely due to higher initial ACVs and lower expansion potential, as these often sell comprehensive platforms rather than individual seats or usage tiers.

Lesson 2: Win with Strong Margins

While ARR and growth rate are vital, they don’t fully reflect a company’s operational health. Two companies with identical growth rates and revenue can have drastically different underlying performance if one spends significantly more on sales and marketing.

To truly understand a cloud company’s performance, it’s essential to examine costs and expenses. Key metrics include gross margins and free cash flow margins, influenced by operating expenses such as sales and marketing, research and development, and general and administrative costs. This lesson delves into these expenses to help you establish appropriate margin targets for your scale.

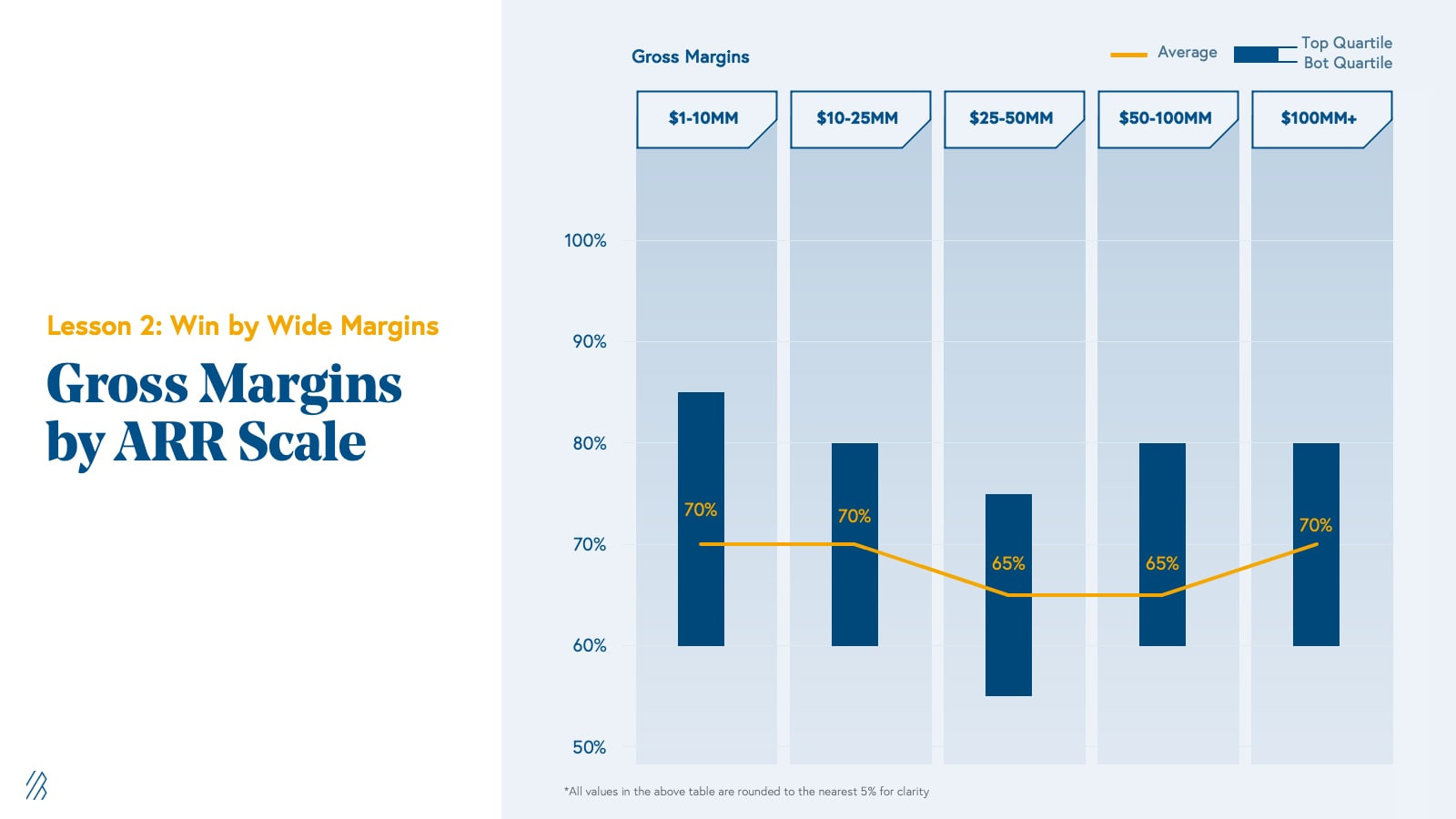

Gross Margin: The Efficiency of Delivery

Software’s inherent advantage lies in its near-zero marginal cost of replication and distribution. Gross margin, calculated as revenue minus cost of goods sold (COGS) divided by revenue, is a critical metric for cloud companies, indicating the efficiency of software delivery. The goal is to maximize gross margin, reflecting minimal marginal cost. High gross margins allow cloud companies to invest more in operating expenses, driving sales, product iteration, and growth. Typical COGS for cloud companies include hosting costs, software implementation costs, and customer success services—all variable costs.

Investors expect cloud companies to maintain gross margins within a tight range due to the low marginal cost of software delivery. Average gross margin remains consistently between 65-70% across different maturity stages, with the middle 50% ranging from ~60-80%.

However, some top-performing cloud companies in our portfolio have operated with gross margins below this range. Twilio, for example, maintained a gross margin of ~50% for much of its early life in the Bessemer portfolio, due to telecom service provider costs in its COGS. Despite this, Twilio remains a leading performer in the BVP Nasdaq Emerging Cloud Index, with a market capitalization exceeding $60 billion.

Gross Margin Benchmarks for Cloud Companies

Gross Margin Benchmarks for Cloud Companies

Operating Expenses: Investing in Growth

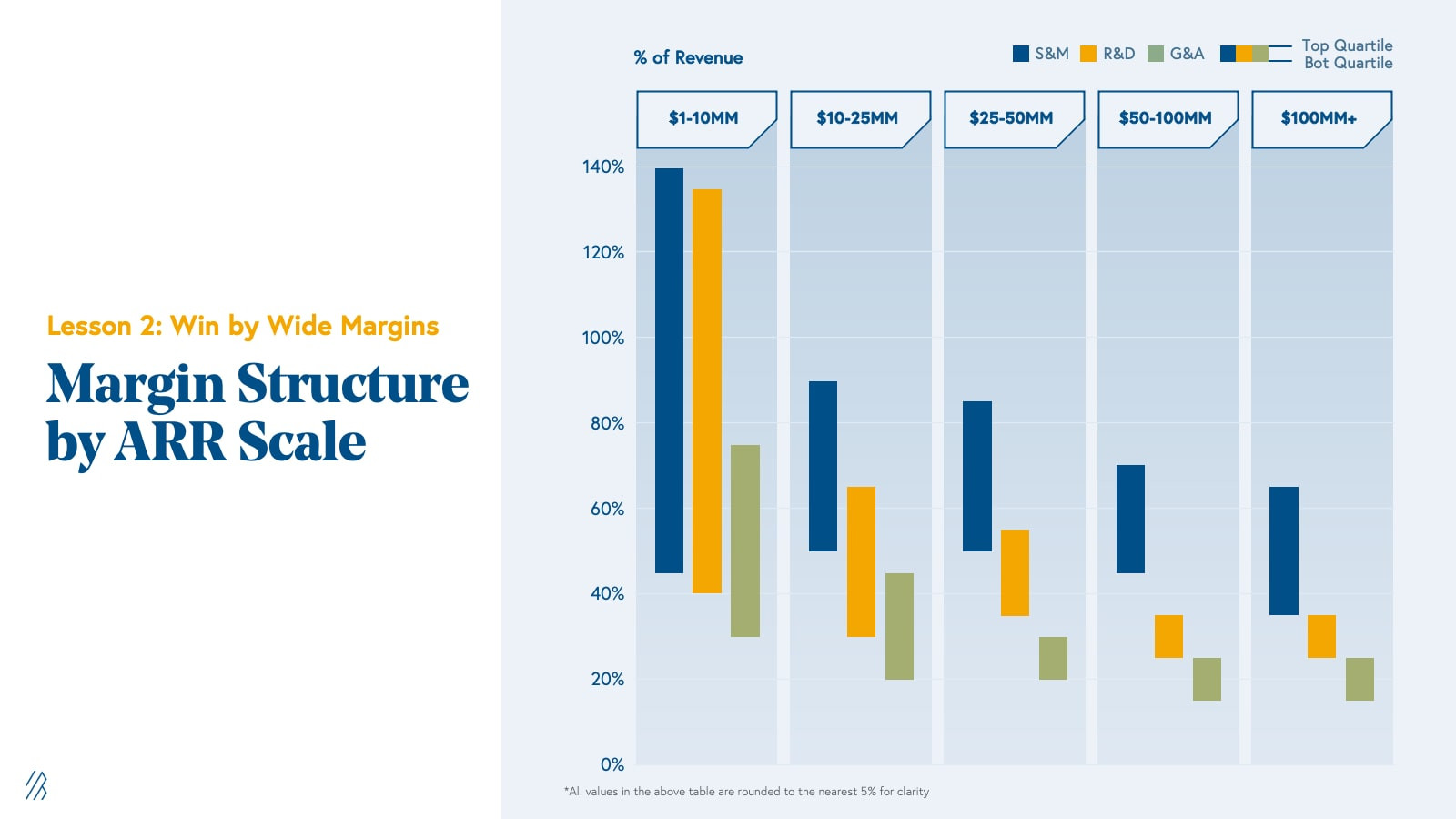

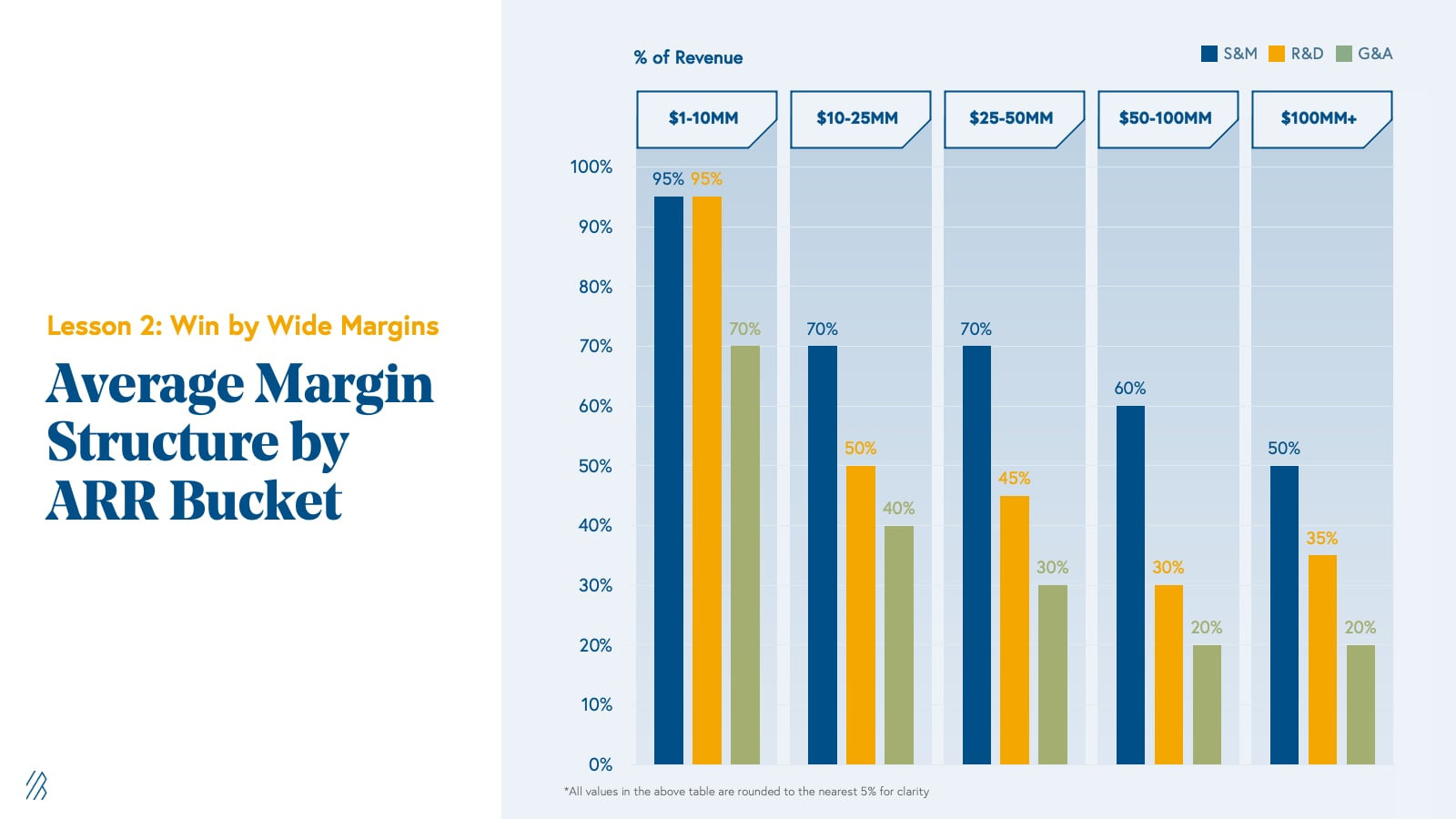

After covering COGS, the remaining gross profit funds operating expenses, with any surplus becoming cash flow. These expenses fall into three main categories: Research & Development (R&D), General & Administrative (G&A), and Sales & Marketing (S&M).

Operating Expense Benchmarks as % of Revenue

Operating Expense Benchmarks as % of Revenue

R&D expense encompasses product-related costs, including product management, development, engineering, and design. It’s the core of a cloud company’s offering and future sales potential. Ironically, R&D is not typically the largest expense driver. It averages 95% of revenue in early years but decreases to 35% by $100MM+ ARR. Initial product investment fuels early growth, but ongoing R&D investment doesn’t scale linearly with revenue. While product enhancements and new product lines require investment, maintaining and improving the core product becomes proportionally less expensive over time. For instance, when we invested in PagerDuty in 2014, R&D expense was nearly 60% of revenue; by IPO, it was around 35%.

General & Administrative (G&A) expense covers back-office functions like executive leadership, finance, legal, compliance, HR, and IT, as well as external costs for legal services, travel, and auditing. G&A is initially high as a percentage of revenue due to establishing these functions and hiring key leaders. However, G&A costs decrease significantly as these functions reach a growth plateau. Regardless of company size, there is only one CFO. Average G&A expense drops from 70% of revenue at $1-10MM ARR to just 20% at $50MM+ ARR.

Sales & Marketing (S&M) expense is the most critical operating expense for cloud investors and founders. It includes sales expenses, compensation, content and brand marketing, demand generation, and sales-related customer success costs. S&M represents the largest cost center, consistently exceeding 50% of annual revenue, even at scale, as sales and marketing talent scales more linearly with revenue growth.

Sales & Marketing Expense Benchmarks as % of Revenue

Sales & Marketing Expense Benchmarks as % of Revenue

For example, when we invested in Adaptive Insights in 2013, the company spent almost 90% of revenue on S&M to drive rapid growth.

CAC Payback: Measuring Sales Efficiency

Sales efficiency is capital efficiency.

Given S&M’s significant revenue share in cloud, sales efficiency directly translates to capital efficiency. Rational burn rates in cloud companies are impossible without efficient sales and marketing. Customer Acquisition Cost (CAC) Payback is a key metric for evaluating S&M efficiency. It measures the time required to recoup customer acquisition costs through gross margin-adjusted ARR. CAC typically includes sales, marketing, and customer success expenses related to renewals, upsells, and cross-sells. Profit generation from a customer only begins after the CAC payback period. Before payback, you are simply recovering acquisition costs. We measure CAC payback against gross margin-adjusted ARR because variable costs associated with cloud software sales do not contribute to profit.

CAC Payback Benchmarks by ARR Range

CAC Payback Benchmarks by ARR Range

Average CAC payback in the $1-10MM ARR range is 15 months, gradually increasing over time. Early adopters are typically cheaper to acquire, and competition increases as companies mature, requiring higher S&M spending. However, by $100MM+ ARR, successful cloud businesses typically optimize their go-to-market model, aligning S&M expense with strong Customer Lifetime Values (CLTVs). CLTV represents the gross margin-adjusted value of a customer over their relationship with the business. A higher CLTV and longer customer lifetime justify higher CAC. CLTV/CAC ratio provides guidance on acceptable CAC levels. Customers become profitable only when CLTV/CAC exceeds 1x. We recommend investing in customer acquisition when CLTV/CAC is 3x or higher. Below that threshold, further experimentation is needed to improve unit economics.

While averages across Bessemer’s cloud portfolio are presented, CAC paybacks can vary significantly, primarily due to customer segment. SMB-focused cloud companies should target shorter CAC payback periods.

Regardless of customer segment, shorter CAC payback periods are always preferable, as customer profitability begins only after CAC is recovered.

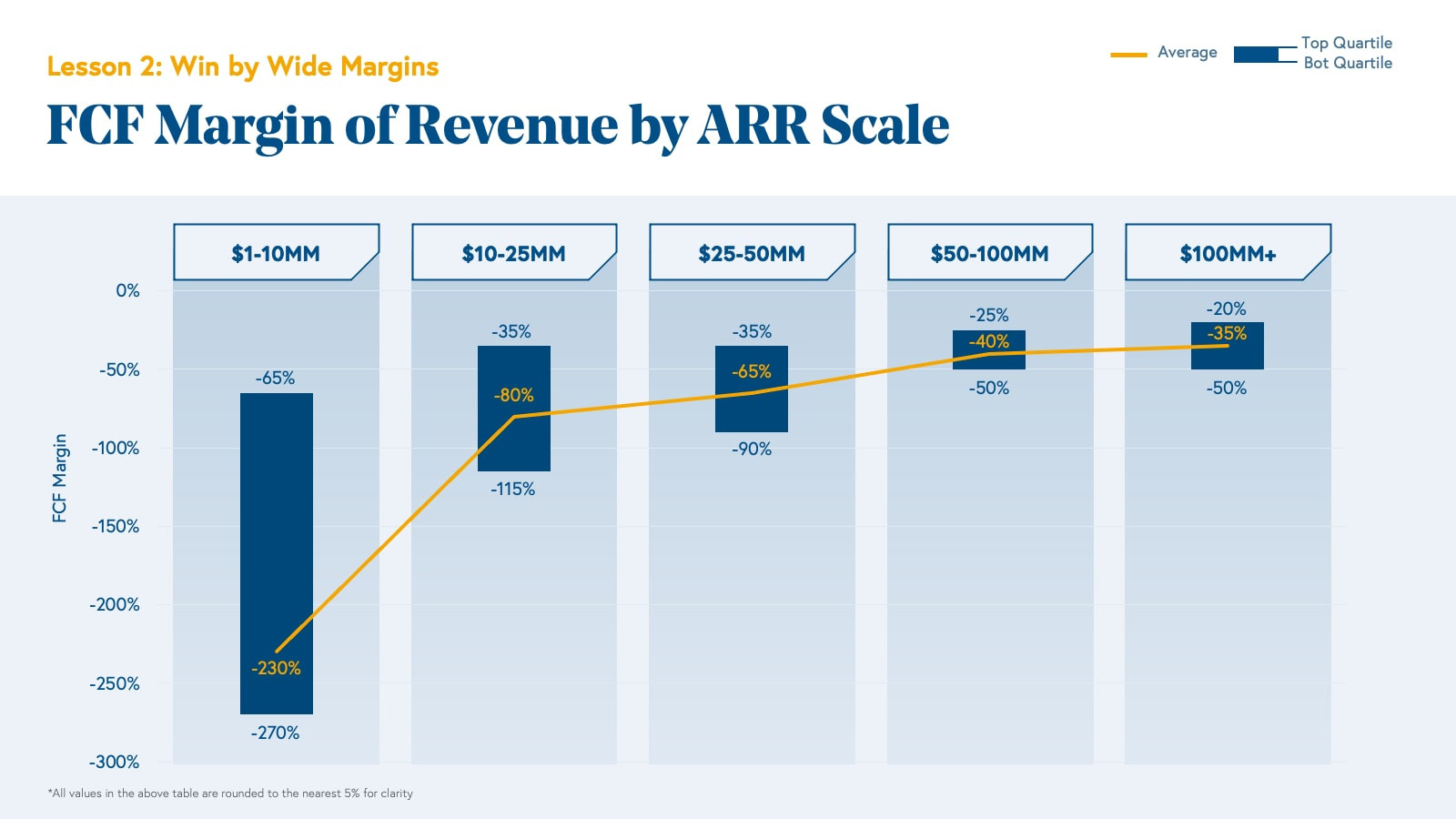

Free Cash Flow Margin: Gauging Profitability

Free cash flow (FCF) represents a company’s cash generation or loss after accounting for COGS, operating expenses, capital expenditures, and adding back non-cash expenses. FCF is crucial because it determines a company’s runway without external capital, especially for cash-burning businesses. For cash-generating businesses, FCF can be reinvested for growth or distributed to shareholders. FCF margin, calculated as cash flow divided by revenue, is a core cloud KPI, indicating profitability and capital efficiency. Investors prioritize prudent capital consumption for product, go-to-market, and administrative needs.

While cash generation is desirable, aggressive spending to drive revenue growth may sometimes be prioritized over immediate profitability in the cloud economy. Investors often weigh ARR growth against burn rate to assess capital efficiency, sometimes favoring growth over profitability.

For instance, at IPO, the top quartile of BVP Nasdaq Emerging Cloud Index companies were at cash flow breakeven. Snowflake, however, burned over $100MM but achieved nearly $170MM revenue growth and over 170% YoY growth, placing it in the top quartile for growth.

Free Cash Flow Margin Benchmarks by ARR Range

Free Cash Flow Margin Benchmarks by ARR Range

Efficiency Score: Balancing Growth and Profitability

When evaluating burn rate, it’s crucial to consider it in the context of growth. A $100MM annual burn rate might seem high, but if it generates $1 billion in net new ARR, it becomes justifiable. The efficiency score helps assess cash consumption relative to revenue generation. It’s calculated as FCF margin plus ARR year-over-year growth rate and is most meaningful after reaching $25MM+ ARR. We advise Bessemer portfolio companies to target a 70% efficiency score between $25-50MM ARR and a slightly lower 50% at $100MM+ ARR, as YoY growth naturally slows and companies balance profitability with aggressive growth.

Efficiency score = FCF margin of ARR + ARR YoY Growth Rate

Younger companies typically exhibit higher growth and burn rates, while mature companies have lower growth and burn (and potentially positive cash flow). The “Rule of 40” suggests a minimum efficiency score of 40%+, but the average BVP Nasdaq Emerging Cloud Index efficiency score is closer to 50%, driven by high performers like Zoom, Shopify, Datadog, and Crowdstrike. Shopify, even with $3.8 billion LTM revenue, maintains ~60% YoY growth and ~10% FCF margins, resulting in a ~70% efficiency score.

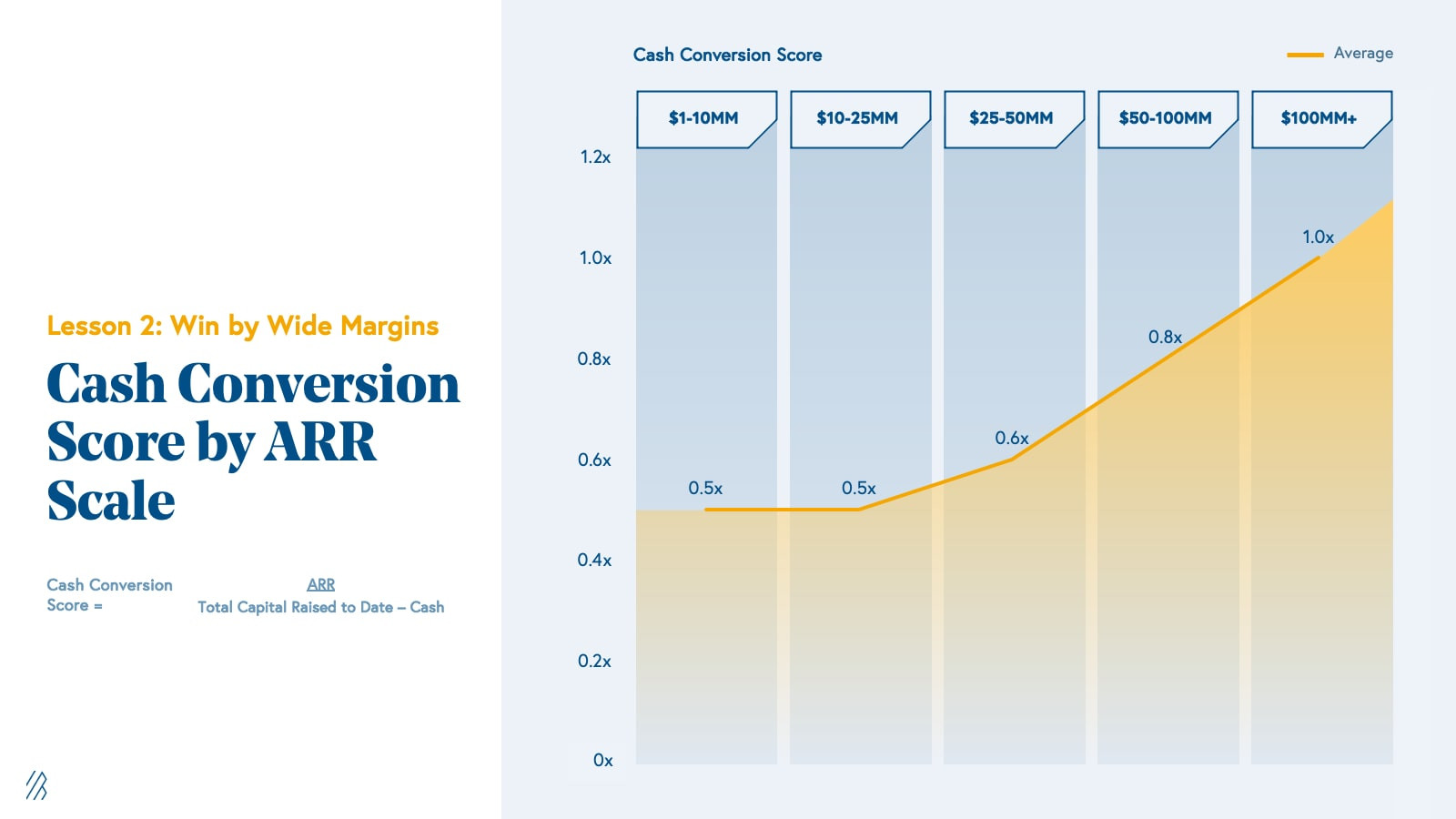

Cash Conversion Score: Return on Investment

The Cash Conversion Score (CCS) evaluates the return generated from capital invested in cloud companies. It’s the ratio of ARR to total invested capital minus cash, effectively representing the ROI of each dollar invested. For both founders and investors, CCS is a powerful indicator of returns. A CCS of 1.0x means each dollar invested yields one dollar of recurring revenue. Assuming a 10x revenue multiple (in line with historical norms), this translates to a $10 enterprise value return for each dollar invested. A 0.1x CCS would only return the invested capital. CCS, while not directly driving ROI, reflects multi-year trends in product-market fit and sales & marketing scalability, making it a key performance indicator.

Average CCS for cloud companies increases with maturity, from ~0.5x at $1-10MM ARR to nearly 1x at $100MM+. Revenue generation often lags spending, and only the strongest companies reach the $100MM+ mark where they leverage their operating model most effectively.

Zapier, a Bessemer portfolio company, stands out with a best-in-class CCS. Having raised only $1.3MM, it announced exceeding $140MM ARR in March 2021. While not every company reaches this level of efficiency, we seek companies with best-in-class CCS of 1x+.

Cash Conversion Score Benchmarks by ARR Range

Cash Conversion Score Benchmarks by ARR Range

Lesson 3: Know Your Valuation

A frequent question from founders to investors and board members of emerging cloud companies is: “What is our company worth?”

Company valuation matters to various stakeholders for different reasons. For founders, higher valuations mean less dilution and greater capital-raising capacity. For potential employees, lower valuations might signal more upside and career growth potential. For current employees, higher valuations increase the value of stock options. However, like private company metrics, private company valuations are often opaque. This lesson explores private cloud company valuations, examining valuation multiples, round sizes, and dilution.

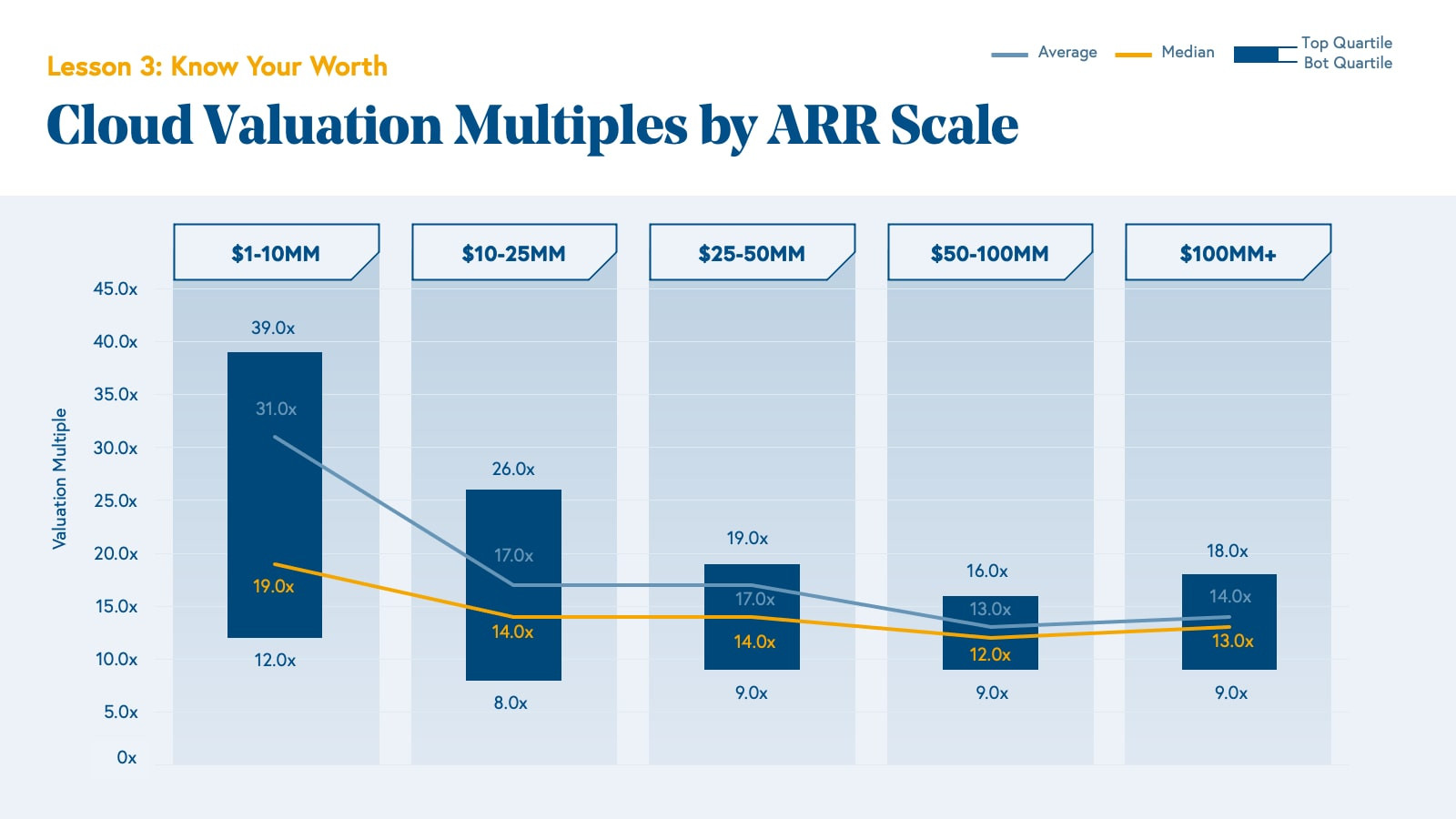

Valuation Multiples: Driven by Growth

For cloud founders seeking VC funding, understanding valuation multiples is crucial. In cloud, valuation is primarily driven by growth. Private investors are generally willing to pay a premium relative to current ARR, betting on future growth to justify valuations. Higher growth rates accelerate a company’s “grow-into” its valuation, justifying higher multiples. For example, a company growing at 300% YoY effectively reduces a 40x valuation multiple to a 10x multiple in just one year. Consequently, higher growth rates command higher multiples. As growth rates naturally decrease across ARR stages, later-stage companies typically raise capital at lower valuation multiples. However, companies sustaining 100% growth at scale command premium valuations.

Over the past decade, Bessemer portfolio cloud companies have averaged over 30x ARR valuations between $1-10MM ARR, decreasing to around 15x ARR beyond $10MM+. While the past decade’s valuation environment was more conservative than 2021, as detailed in the Cloud 100 2021 Benchmarks Report, the average Cloud 100 multiple in 2021 was 34x (up from 9x in 2016). Over a decade-long perspective, the middle 50% of cloud companies were priced at ~10-20x ARR. Unlike the Cloud 100, this dataset isn’t limited to the top 100 cloud companies annually.

Valuation Multiples Benchmarks by ARR Range

Valuation Multiples Benchmarks by ARR Range

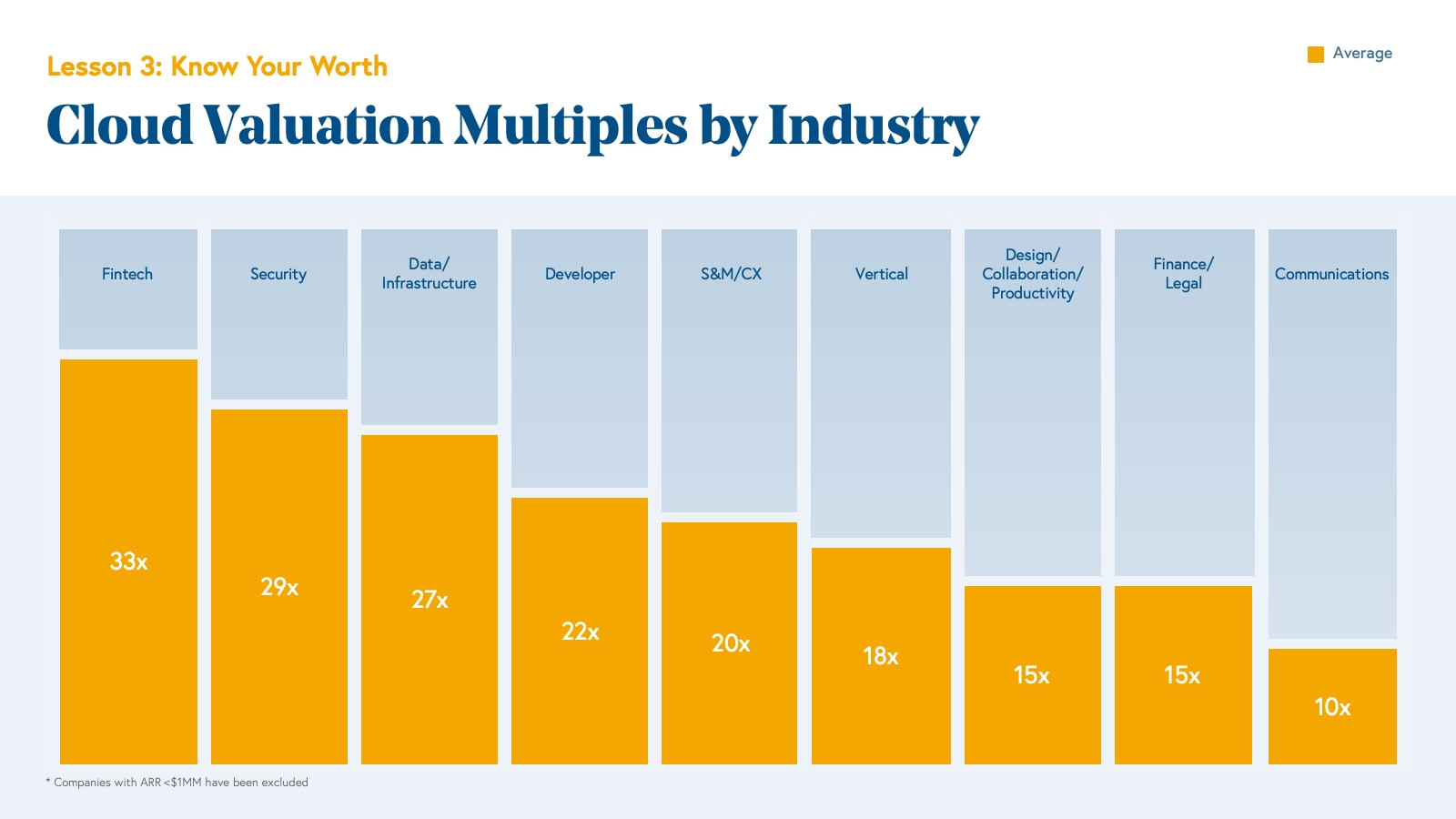

Valuations can vary significantly across industries, often due to TAM size and industry-specific growth rates. Fintech has commanded the highest average multiples in the Bessemer portfolio over the past decade (33x), followed by security (29x) and data infrastructure (27x). However, multiples as high as 50x and 100x have been observed in all three categories.

Valuation Multiples Benchmarks by Industry

Valuation Multiples Benchmarks by Industry

Currently, the cloud valuation environment has undergone a step-function change, largely due to increased capital inflow, strong investor demand, and ongoing tailwinds boosting growth rates. Analyzing Bessemer portfolio cloud companies that transacted between 2020-2021 reveals a valuation multiple of approximately 20x the growth rate.

Valuation Multiples vs. Growth Rate (2020-2021)

Valuation Multiples vs. Growth Rate (2020-2021)

Round Size and Dilution: Balancing Capital and Ownership

Round size is another key factor in structuring fundraising. Balancing dilution with sufficient runway is a constant challenge.

As companies demonstrate growth, fundraising becomes easier.

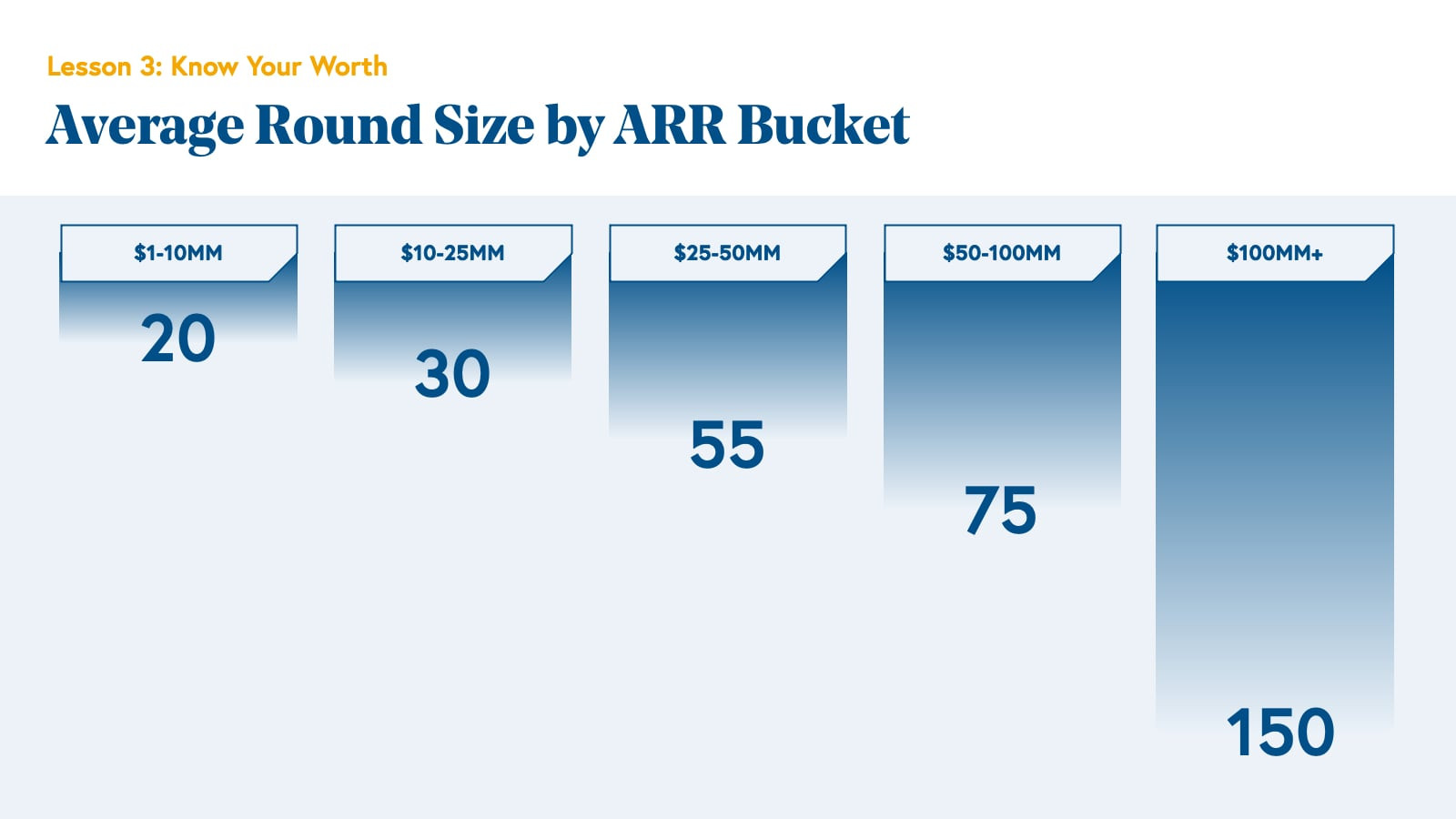

Access to capital is crucial for cloud company success, enabling hiring and growth investments. Cloud companies, due to their negative initial cash flow dynamics, often rely on capital markets for operational runway. Ironically, fundraising becomes easier as companies prove their growth potential. Capital access is greatest for those who need it least. As companies mature, round sizes tend to increase. Investors are more willing to invest larger sums as risk decreases, and companies are more willing to accept larger rounds with less dilution.

Data confirms this trend: round sizes increase with revenue. Average round size for Bessemer cloud companies from $0-10MM ARR is $20MM, increasing to over $75MM for companies at $50-100MM ARR. Interestingly, while ARR buckets increase non-linearly, round sizes increase linearly, indicating that larger companies are not raising proportionally larger rounds relative to ARR size. While this data spans a decade of Bessemer investments, recent increases in round sizes in 2020 and 2021 exceed even these averages.

Average Round Size Benchmarks by ARR Range

Average Round Size Benchmarks by ARR Range

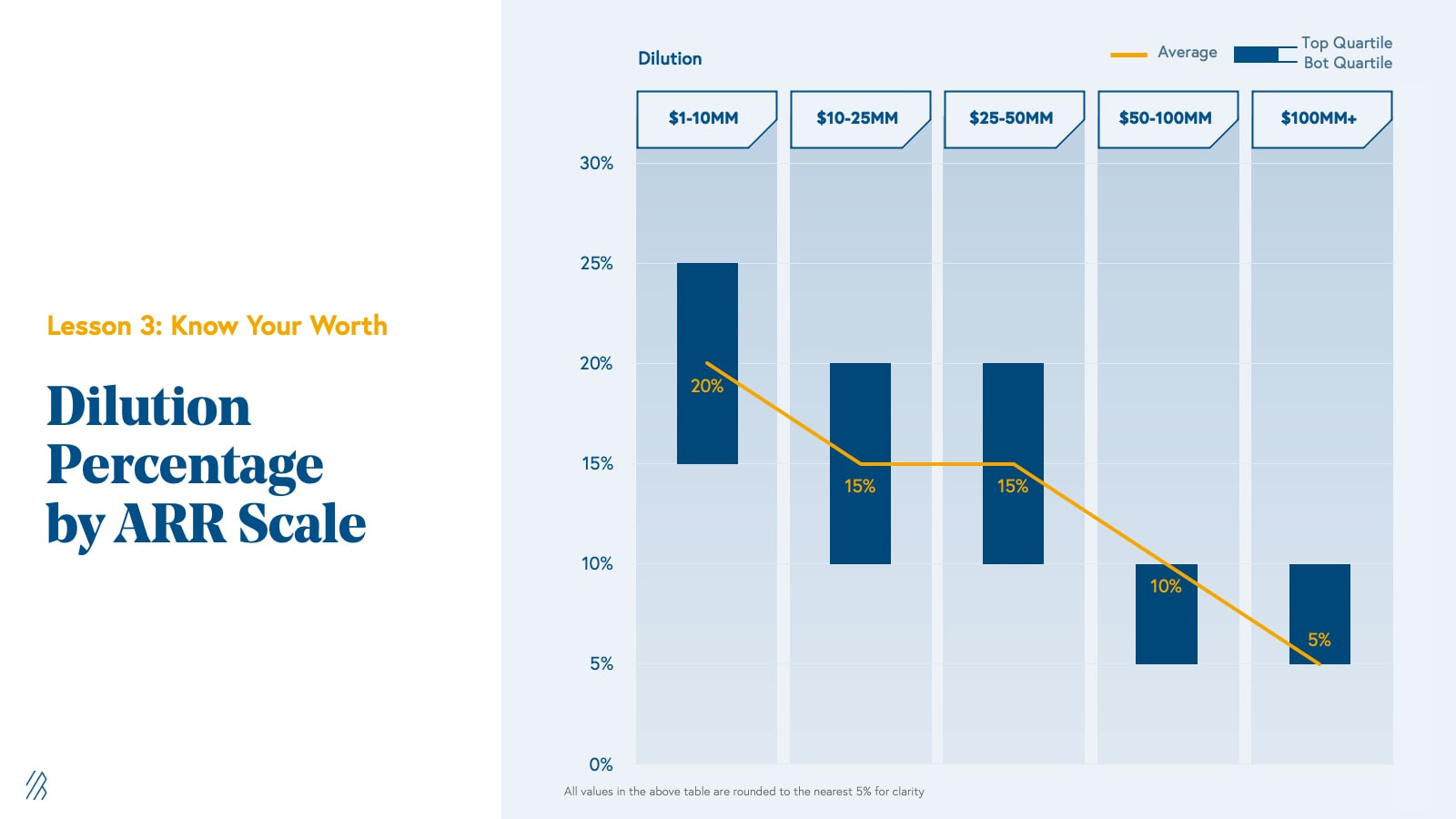

As company valuations increase with maturity, founders understandably sell less equity for the same capital amount. Dilution decreases with scale. From $1-10MM ARR (Series A or B), companies typically sell about 20% of their equity. By $100MM ARR (Series E or F), dilution decreases to just over 5%.

Average Dilution Benchmarks by ARR Range

Average Dilution Benchmarks by ARR Range

Lesson 4: The TL;DR – Chart Your Course to the Next Milestone

Building a business is a challenging journey with both highs and lows. We’ve witnessed this firsthand with category-defining companies like Toast, Shopify, Twilio, Procore, and PagerDuty. We are sharing this proprietary data to provide benchmarks for founders to guide their business development and understand key targets.

The following sections outline specific metrics that founders, CEOs, CFOs, and board members should track, based on Bessemer’s decade-long portfolio research and experience. While achieving these milestones requires dedicated effort, we aim to provide a clear picture of the goals cloud companies should pursue.

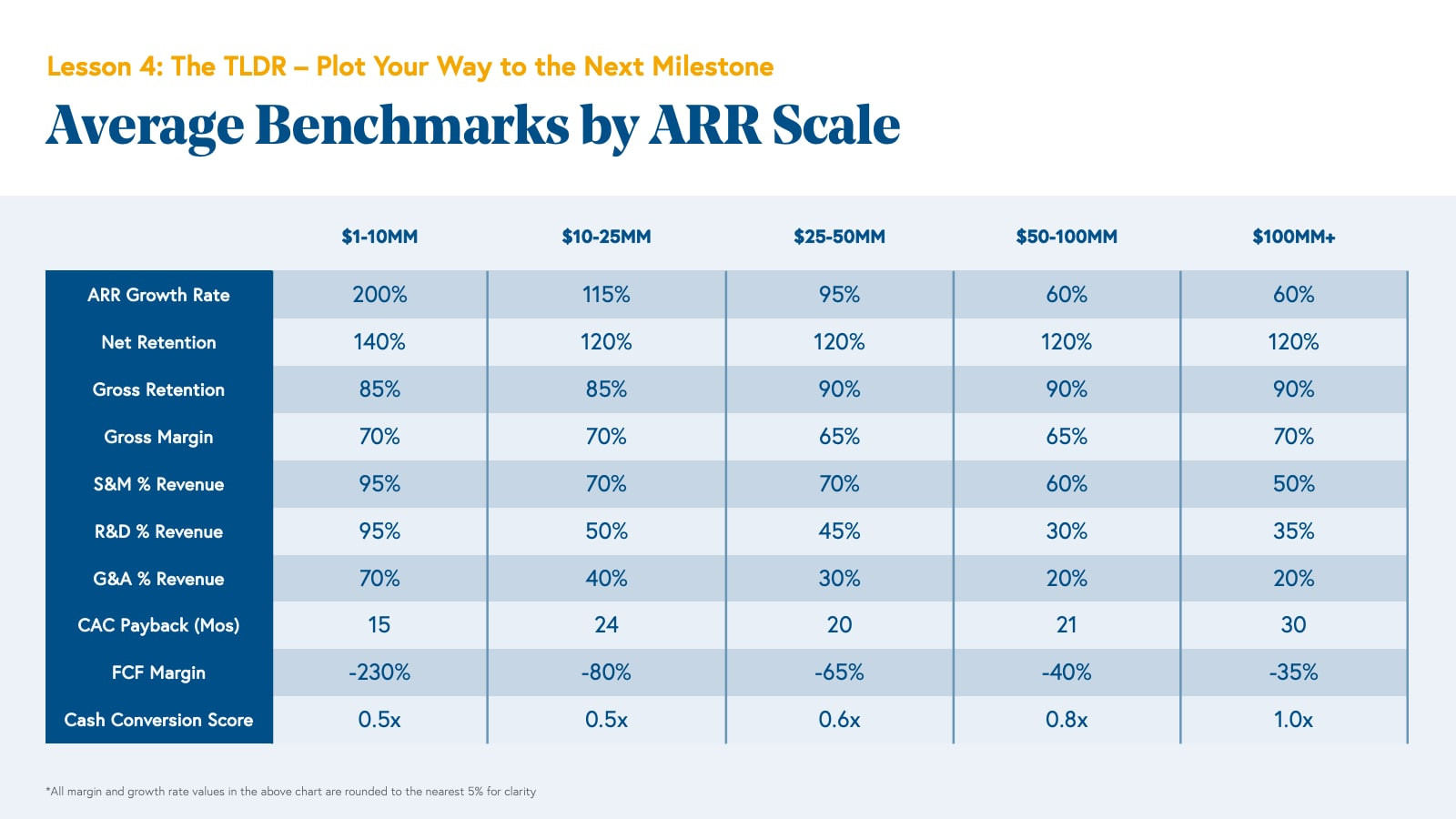

Average Benchmarks by ARR Scale

Average Benchmarks Across ARR Ranges

Average Benchmarks Across ARR Ranges

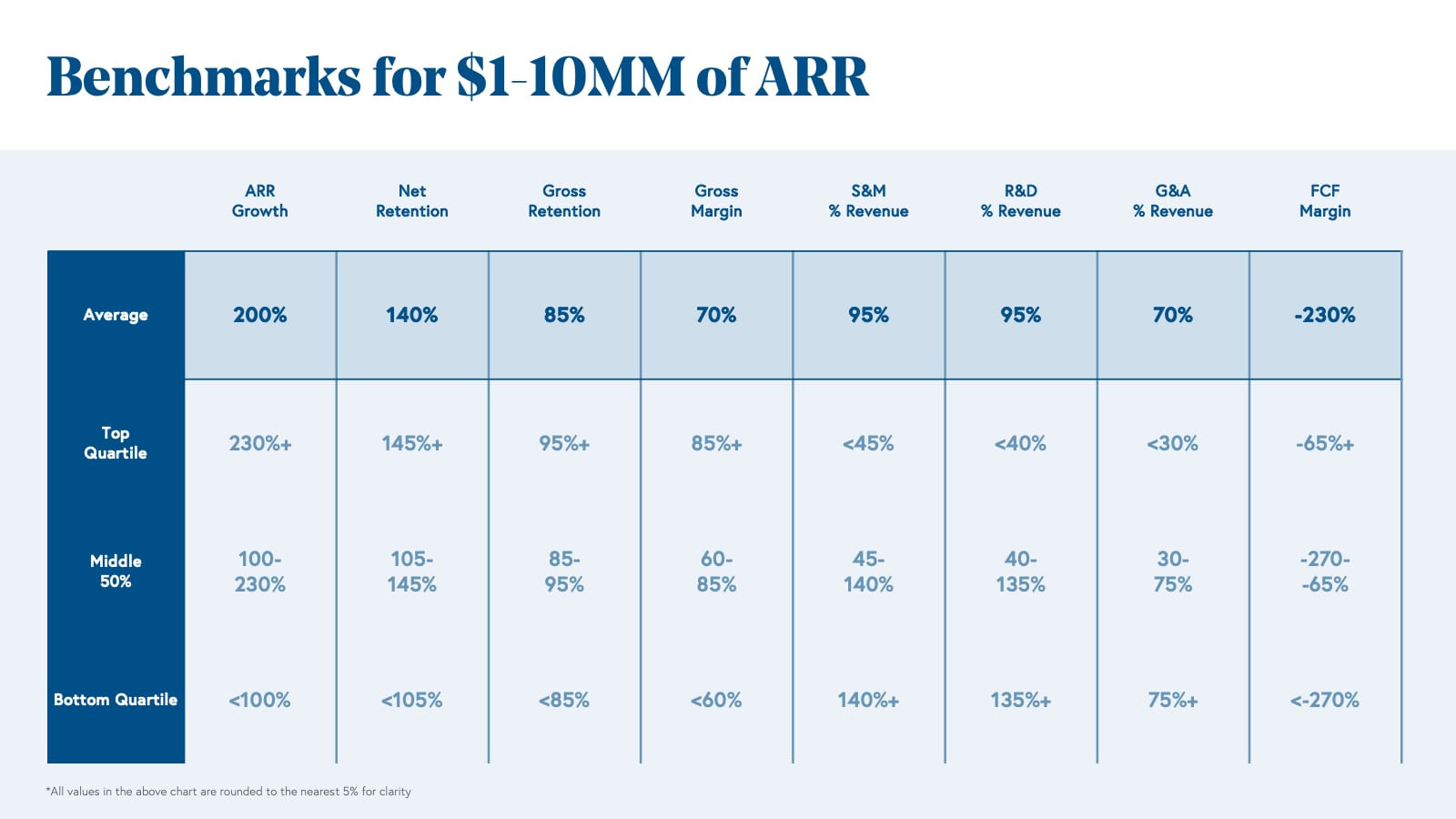

Benchmarks for Companies with $1-10MM ARR

Top-performing cloud companies in the $1-10MM ARR range exhibit ARR growth rates exceeding 230%, Net Retention above 145%, Gross Margins over 85%, and FCF margins better than -65%.

Benchmarks for -10MM ARR Companies

Benchmarks for -10MM ARR Companies

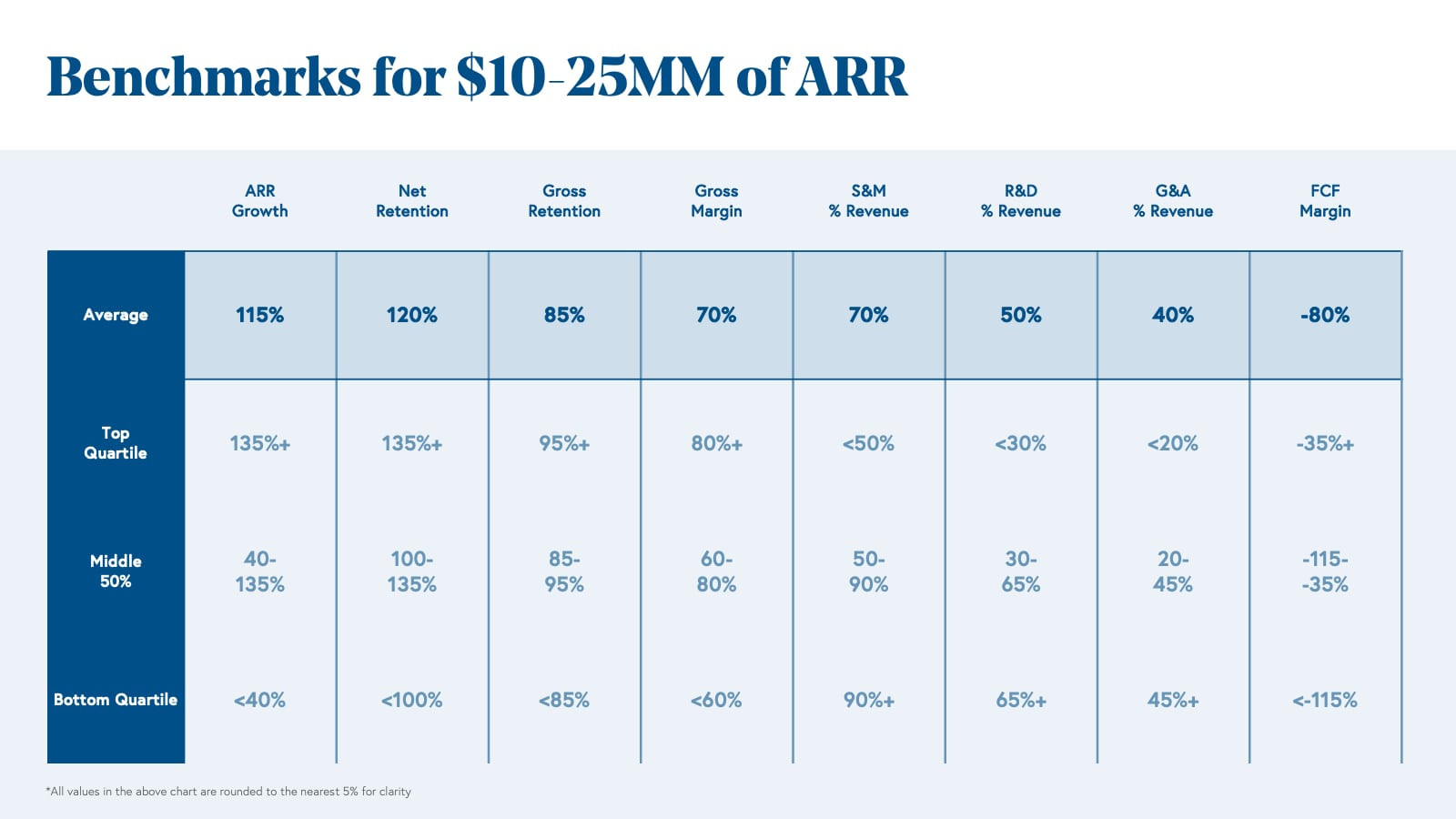

Benchmarks for Companies with $10-25MM ARR

Top-performing cloud companies in the $10-25MM ARR range show ARR growth rates exceeding 135%, Net Retention above 135%, Gross Margins over 80%, and FCF margins better than -35%.

Benchmarks for -25MM ARR Companies

Benchmarks for -25MM ARR Companies

Benchmarks for Companies with $25-50MM ARR

Top-performing cloud companies in the $25-50MM ARR range demonstrate ARR growth rates exceeding 110%, Net Retention above 130%, Gross Margins over 75%, and FCF margins better than -35%.

Benchmarks for -50MM ARR Companies

Benchmarks for -50MM ARR Companies

Benchmarks for Companies with $50-100MM ARR

Top-performing cloud companies in the $50-100MM ARR range achieve ARR growth rates exceeding 80%, Net Retention above 135%, Gross Margins over 80%, and FCF margins better than -25%.

Benchmarks for -100MM ARR Companies

Benchmarks for -100MM ARR Companies

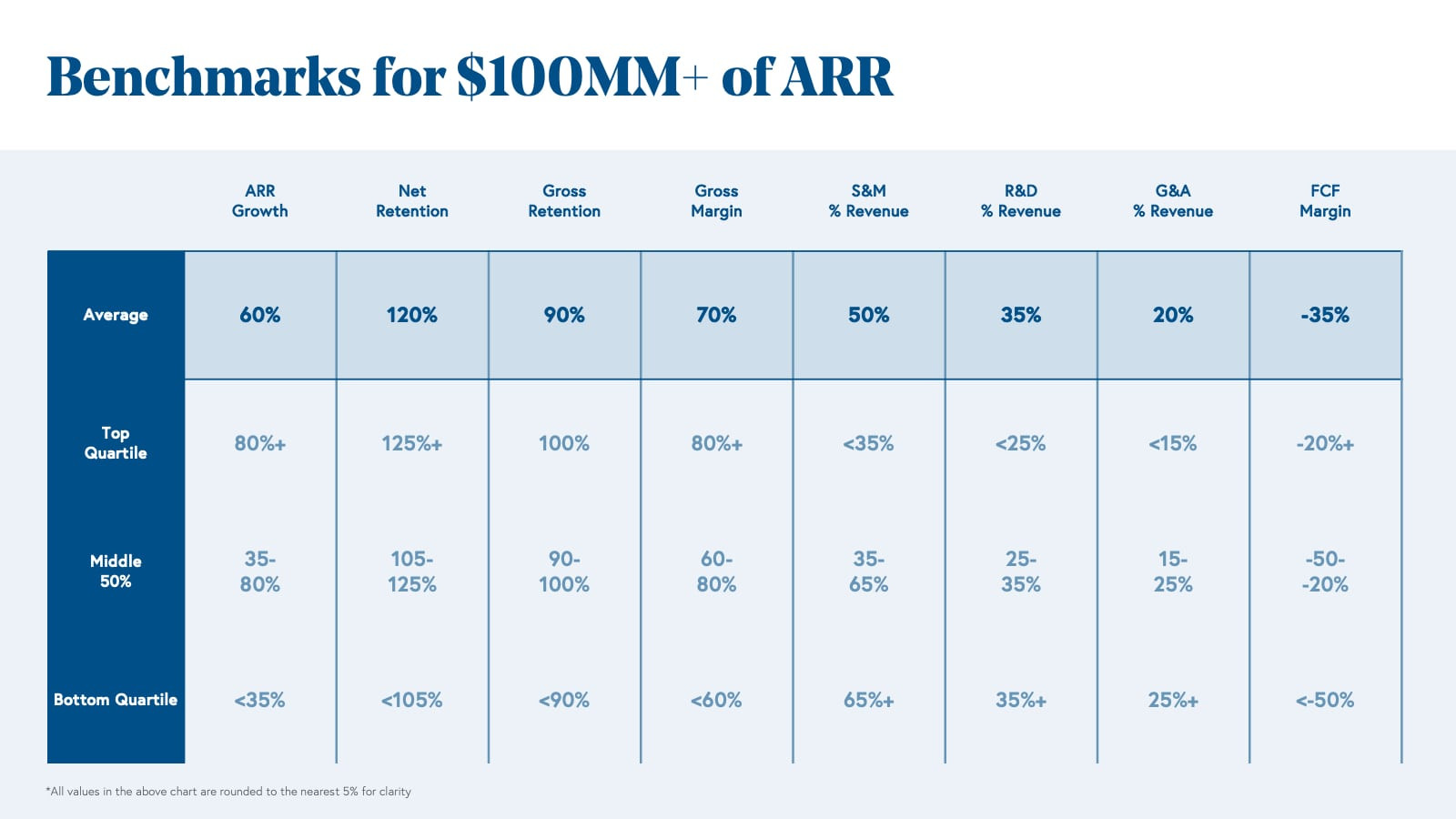

Benchmarks for Companies Growing Beyond $100MM ARR

Top-performing cloud companies growing beyond $100MM ARR sustain ARR growth rates above 80%, Net Retention over 125%, Gross Margins over 80%, and FCF margins better than -20%.

Benchmarks for Companies Beyond 0MM ARR

Benchmarks for Companies Beyond 0MM ARR

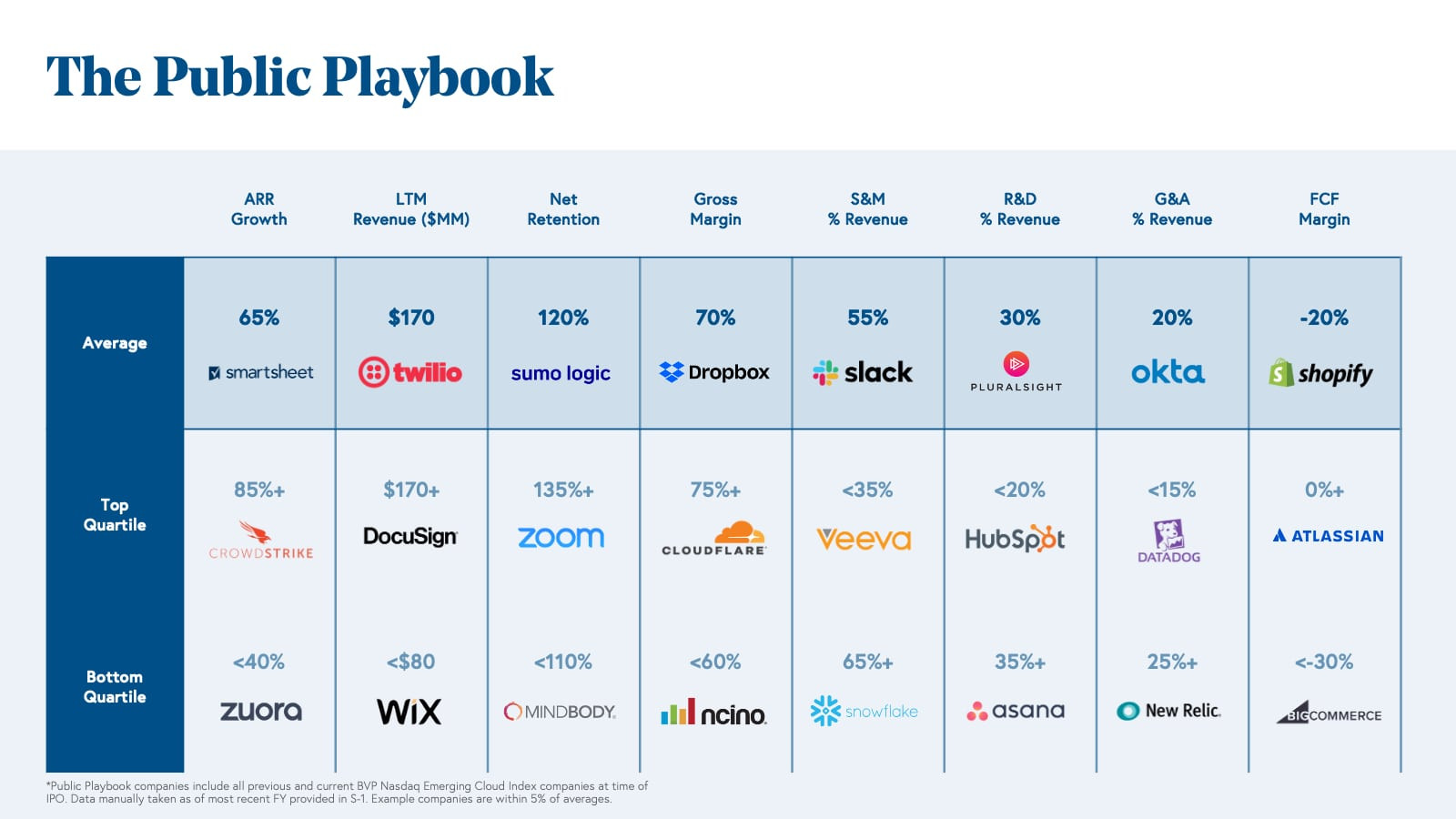

Bonus Lesson 5: Beyond $100MM – Adopt the Public Company Playbook

What happens after reaching $100MM ARR? Similar to our “Public Playbook” bonus lesson in the 10 Laws of Cloud, we revisit it here.

Building a cloud company often includes the aspiration of going public. At Bessemer, we partner with founders with long-term visions, aiming for public company status. While M&A opportunities may arise, our investment thesis centers on companies becoming standalone public platforms. You are likely building your company to impact the world and envision ringing the NYSE or Nasdaq bell.

So, what lies beyond $100MM ARR? We’ve compiled benchmarks for Bessemer’s public cloud index companies, tracked by the BVP Nasdaq Emerging Cloud Index, mirroring the private cloud benchmarks. These are the metrics that companies like Toast, Amplitude, and Freshworks have targeted in preparation for their IPOs.

Consistent with the $100MM+ ARR benchmarks, public cloud companies at IPO typically exhibit an average LTM revenue growth rate of 65%, net retention of 120%, gross margin of 70%, R&D at 30% of revenue, S&M at 55% of revenue, G&A at 20% of revenue, and FCF margin at -20%.

However, running the public playbook requires sufficient GAAP LTM revenue. The average LTM GAAP revenue for cloud companies in their last fiscal year before IPO was $170MM, with variations ranging from Ellie Mae to Twilio.

Transitioning to the public playbook also necessitates understanding that while private markets prioritize upfront investment and growth, public markets value maturity, operating leverage, and profitability visibility. We recommend cloud companies target IPO only when they project free cash flow positivity within 1-2 years. The top quartile of cloud companies were already at FCF breakeven or positive at IPO, including Atlassian, JFrog, and Zoom.

Adopting the public playbook and striving for these metrics will guide you beyond $100MM ARR and towards life as a public company.

Key Metrics for Public Cloud Companies at IPO

Key Metrics for Public Cloud Companies at IPO

Share Your Metrics

Are you preparing for your next funding round as a venture-backed cloud startup? Download our templates to benchmark your company’s performance as you scale towards $100 million ARR and beyond. Use these tools in your boardroom to track your business growth effectively.

Download Your Bessemer Benchmarks

For questions, deeper metric discussions, or if your company demonstrates best-in-class metrics, please contact Mary D’Onofrio at [email protected].

*Data in this report is based on financial information from Bessemer’s cloud portfolio from 2010-1H21 and is not a random sample of the entire private market.

**Index includes any company currently or previously listed on the BVP Nasdaq Emerging Cloud Index.